Rs 2 Crores is a huge amount, but with the right SIP (Systematic Investment Plan) and patience, it can easily be reached in 10 years with the magic of compounding.

How much one needs to save per month to reach their target becomes the question. However, the way to get that answer will differ according to whether the individual prefers active or passive fund and depends on the expected returns.

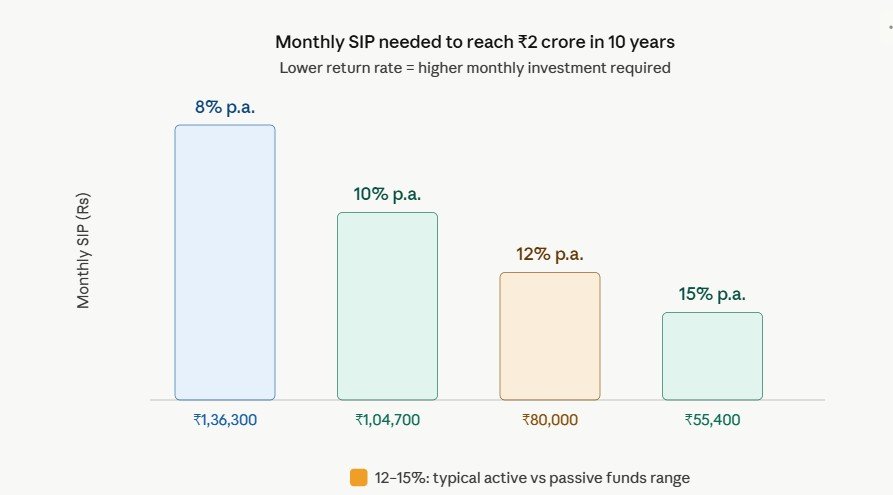

In the illustration below, let me show how one can be a millionaire at the end of 10 years.

What is SIP?

SIP (Systematic Investment Plan) is a type of investment that allows an investor to invest a fixed amount in a mutual fund on a regular basis, typically monthly. It’s similar to saving money with a recurring deposit, but instead of receiving a flat investment from a bank, you’re investing your money in the stock market, where historically your returns will be much greater than if you were just using a savings account.

The key to SIPs is the concept of rupee cost averaging as well as the power of compounding. When the market is down your regular SIP amount will purchase more units of the mutual fund. Conversely, when the market is up your total units will appreciate in value. By having a ten year time horizon, you will be averaging out the market volatility and building wealth on a regular basis.

Your rate of return is determined by the mutual fund you choose or what conversation you are having regarding an active or passive fund. This is where the current discussion between active and passive funds becomes extremely important.

Active Vs. Passive Funds

When you choose a fund for SIPs (Systematic Investment Plans), matching funds is greatly reduced to either an active or passive fund option.

Active funds are managed by professional fund managers who buy and sell equities upon their discretion in an effort to outperform a designated index or benchmark. On average, active funds charge 1%-2.5% in management fees. Thus, the goal of investing in an active fund is to receive a total return that is higher than the average of the benchmark over time.

Passive funds simply track a broad market index (such as the Nifty 50 or the Sensex); therefore, they will not outperform their respective indexes. Additionally, passive funds have lower management fees (0.1%-0.5%) than active funds. Many financial experts suggest that, after factoring in fees, you will be better off with a passively managed fund over time than with an actively managed fund.

Why is this important to your goal of accumulating 2 crores? The difference between a 10% and 14% return on investment — the difference between below-average performing active funds and superior performing active funds — means that you will have to save or invest tens of thousands of rupees more each month to reach your goal. Simply put, choosing between an active versus a passive fund will directly affect your finances.

The Core Calculation: What Return Rate Are You Expecting?

Here’s where the real math comes in. The formula used for SIP calculations is based on the future value of a recurring investment:

FV = P × [(1 + r)^n – 1] / r × (1 + r)

Where:

- FV = Future Value (Rs 2,00,00,000 in our case)

- P = Monthly SIP amount

- r = Monthly rate of return (annual rate ÷ 12)

- n = Number of months (120 months for 10 years)

Let’s look at what this spits out at different return assumptions.

Monthly SIP Required at Different Return Rates

At 8% Annual Returns (Conservative)

If you’re investing in debt-oriented hybrid funds, conservative balanced funds, or underperforming active funds, you might realistically expect around 8% per annum. At this rate, you’d need approximately:

Monthly SIP ≈ Rs 1,36,300

That’s a chunky amount, honestly! This is what happens when your returns are modest — compounding doesn’t have enough firepower to do the heavy lifting. Passive funds invested purely in debt wouldn’t typically hit this corpus target either, making fund selection crucial.

At 10% Annual Returns (Moderate)

At 10% annual returns — which is roughly what a conservative equity-heavy passive index fund might deliver over a decade — the required monthly SIP drops to:

Monthly SIP ≈ Rs 1,04,700

Still over a lakh per month, but noticeably lower. Many large-cap passive funds tracking the Nifty 50 have historically delivered returns in this ballpark, though of course past performance doesn’t guarantee future results.

At 12% Annual Returns (Active vs Passive Funds Battleground)

Here’s where the active vs passive funds debate really heats up! A well-performing active fund or a mid-cap index fund might realistically target 12% per annum. At this level:

Monthly SIP ≈ Rs 80,000

Now we’re talking! That’s a number many upper-middle-class Indian families can actually consider. A flexi-cap active fund that consistently beats the index, or even a Nifty Next 50 passive fund, could realistically get you into this territory.

At 15% Annual Returns (Optimistic but Possible)

Good small-cap active funds and some mid-cap active managers have historically delivered 15%+ over 10-year periods, though this isn’t guaranteed. If you’re lucky (and skilled at fund selection), you might achieve:

Monthly SIP ≈ Rs 55,400

That’s a massive difference from the 8% scenario! Just under Rs 56,000 per month versus Rs 1.36 lakh per month — for the same Rs 2 crore end goal. This is why the active vs passive funds conversation matters so deeply when you’re playing the long game.

Stepping Back: What Kind of Investor Are You?

So, which number applies to you? Well, that depends entirely on where you’re putting your SIP money. And here’s where you’ve got to make some honest decisions about the active vs passive funds debate for your own situation.

If you’re a hands-off investor who’d rather not agonise over quarterly fund manager updates and NAV movements — passive index funds might be your best friends. They won’t make you rich overnight, but they’ll give you steady, reliable growth with minimal effort and low costs. Think of them as the “set it and forget it” school of investing.

If you’re willing to do your homework, track fund performance, evaluate fund managers, and make occasional switches when a fund starts underperforming — certain active funds could potentially deliver the extra 2-4% per annum that makes a significant difference to your final corpus.

The active vs passive funds question, ultimately, isn’t about which is universally “better.” It’s about which fits your investing temperament, time availability, and risk appetite.

The Impact of Stepping Up Your SIP Every Year

Here’s a little secret that most beginner investors don’t know about: you don’t have to start with a big SIP amount. Many mutual fund platforms allow something called a Step-Up SIP (also known as Top-Up SIP), where you increase your monthly contribution by a fixed percentage each year.

If you start with Rs 50,000 per month today and increase it by 10% every year, you’ll be surprised at how quickly you approach the 2-crore mark without ever having to start with a massive outlay.

For example:

- Start: Rs 50,000/month

- After Year 1: Rs 55,000/month

- After Year 2: Rs 60,500/month

- …and so on

With 12-15% returns and annual step-ups, a Rs 50,000 starting SIP could comfortably cross the Rs 2 crore mark in 10 years. This flexibility makes the goal much more accessible — especially for younger professionals whose incomes tend to grow over time.

Active Vs Passive Funds – History

The SPIVA (S&P Indices vs Active) India Scorecards have revealed that, over rolling 10-year periods, a large majority of active large-cap funds have posted returns that fall below benchmark indices, Nifty 50. Approximately 60-80% of large-cap active funds have underperformed by the end of one’s investment horizon (10 years).

What does this tell you? If you are considering investing in a large-cap active fund with an expected nominal return of 14-15%; the actual return could be closer to 10-11%. Therefore, you would need to invest more through monthly SIP.

The active vs passive fund environment, however, is very different for mid-cap and small-cap stocks. Historically, there are many active mid-cap and small-cap fund managers in India that have outperformed their benchmarks more consistently; thereby providing greater justification for the use of active management in this area.

As a result, many astute investors in India employ a strategy involving the use of passive large-cap vehicles and active mid-cap/small-cap vehicles. This hybrid investing model takes advantage of the lower overall costs associated with index-based funds where active management has generally struggled while allowing for the higher potential alpha generated by qualified managers in less efficient markets.

Step by Step Planning

Let’s bring it all together with a practical, step-by-step approach:

- Define your target clearly. You want Rs 2 crore in 10 years. Great — that’s a well-defined goal.

- Assess your current savings capacity. How much can you genuinely set aside each month without straining your budget? Be realistic.

- Choose your fund category. Refer to the active vs passive funds framework above. If you’re starting fresh and don’t want complexity, a 60-70% allocation to passive index funds (Nifty 50 + Nifty Next 50) and 30-40% in a reputed mid/small-cap active fund is a solid starting point.

- Run your numbers. Use the table above as a reference. At 12% blended returns, you need around Rs 80,000/month. Can you manage that? If not, consider stepping up.

- Start a Step-Up SIP. If Rs 80,000 is too high today, start at Rs 50,000 and increase by 10-15% annually. You’ll likely still hit your goal.

- Stay the course. The biggest mistake investors make is stopping their SIPs during market downturns. Don’t. SIPs are designed to work through volatility, not around it.

- Review annually, not monthly. Check your fund’s performance against its benchmark once a year. If a fund has consistently underperformed for 3+ years, consider switching. But don’t panic-sell over short-term dips.

Role of Inflation

What most people tend to ignore is inflation. 2 Crores will not have the same purchasing power today as they do today when looking at the purchase power in 2035. In India, with an average inflation rate around 5-6% per annum, the actual value of your corpus will deteriorate significantly.

Should these considerations lead you to set higher targets? Perhaps, If you want to achieve the equivalent of 2 Crores today in 10 years, your nominal target should be set at approximately 3.2 – 3.5 Crores to offset inflation.

This upward adjustment of all the numbers has a cascading effect on all your other assumptions. For example, when targeting 3.5 Crores at 12% return, you now need around 1.4 Lakhs/Month as opposed to 80,000.

The debate surrounding active versus passive funds will include this. An active fund that can generate returns of 15%+ in a high inflation environment would provide a significantly better return than a passive one that provides returns of 10%, because it preserves your real purchasing power much better.

Conclusion

Saving enough money to create a Rs 2 crore corpus over the course of 10 years is not going to be difficult to achieve if you think about it mathematically. However, depending on how you understand the difference between active versus passive funds as well as how you go about using that knowledge will actually result in significant differences in the solutions you will find to this problem.

For example, if your return is 8%, you will have to save more than Rs 1.36 lacs per month. If you are savvy regarding your selection of funds and utilize the best passive index-type funds for large caps combined with some excellent active management for mid/small type companies, it is possible that you will obtain your target Rs 2 crore corpus with returns between 12%-15%, which means that you will only need to save between Rs 55,000 to Rs 80,000 per month.

The bottom line is to start now, make savvy fund selections, consider using Step-Up SIPs if you cannot save the desire monthly amount immediately, and do not stop saving if the market experiences short-term downturns. The active vs passive fund debate may be critical, but the single most critical decision you will ever make is to simply start saving to create your Rs 2 crore corpus. Your future self will be extremely grateful to you 10 years from now for having made the decision to start today.

{kind=link}