Facing a mountain of debt can feel overwhelming. When bills pile up and creditors keep calling, it’s easy to think bankruptcy is your only way out. But for many people, it doesn’t have to come to that. Credit counseling is a powerful, often overlooked tool that can help you regain control of your finances — without the lasting damage that bankruptcy leaves behind. The best part? Help is more accessible than most people realize.

What Is Credit Counseling?

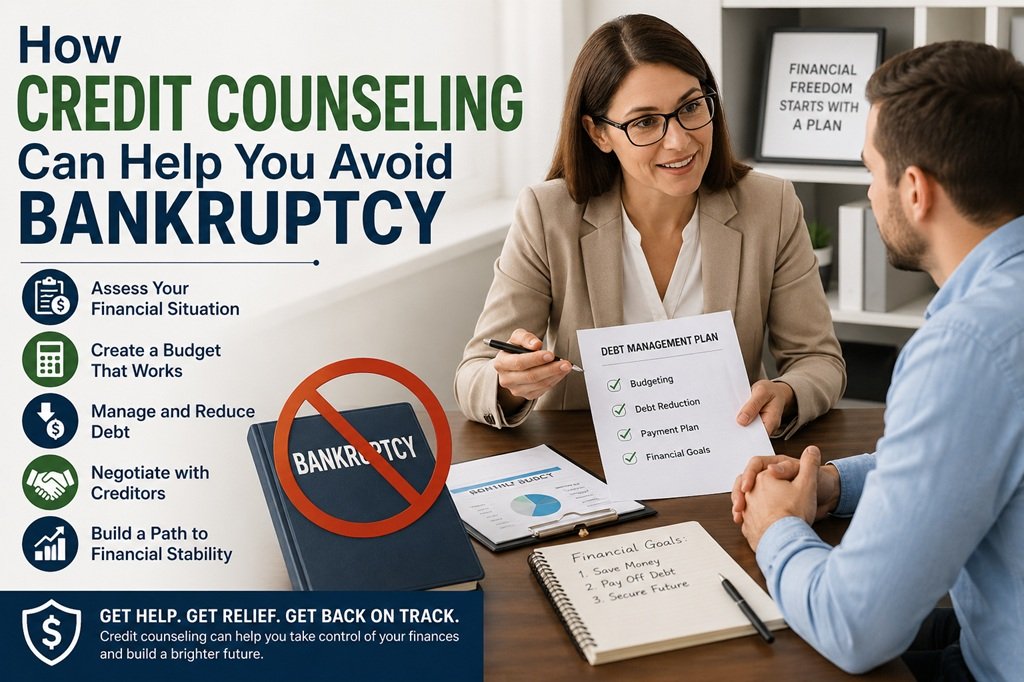

Credit counseling is a service offered by nonprofit agencies that helps people manage debt, build better financial habits, and explore options outside of bankruptcy. A certified credit counselor reviews your income, expenses, and debts to give you a clear picture of where you stand. From there, they work with you to create a realistic plan to move forward.

It’s not about judgment. It’s about solutions. And for millions of Americans, it has been the turning point that changed everything.

The Real Cost of Bankruptcy

Before you consider filing, it’s worth understanding what bankruptcy actually costs you. Yes, it can wipe out certain debts — but it comes with serious trade-offs.

A bankruptcy filing stays on your credit report for seven to ten years. During that time, getting approved for a mortgage, car loan, or even a credit card becomes significantly harder. Some employers run credit checks as part of the hiring process, meaning bankruptcy could affect your career. There are also legal fees, court costs, and the emotional toll of going through the process.

For many people, these consequences far outweigh the short-term relief.

How Credit Counseling Offers a Different Path

Credit counseling takes a different approach. Instead of walking away from your debt, you work through it — often in a way that’s more manageable than you’d expect.

One of the most common outcomes of credit counseling is enrollment in a Debt Management Plan, or DMP. Through a DMP, your counselor negotiates with creditors on your behalf to reduce interest rates and waive certain fees. You make one monthly payment to the agency, and they distribute it to your creditors. Over time — typically three to five years — you pay off your debt in full.

This approach keeps your credit intact, removes the legal consequences of bankruptcy, and gives you a structured, stress-reducing path out of debt.

Getting Started Is Easier Than You Think

Many people delay seeking help because they assume the process will be complicated or expensive. The truth is, nonprofit credit counseling is often free or very low cost. An initial consultation gives you a complete financial assessment with no obligation.

If you’re not sure where to turn, Consolidated Credit offers credit card debt consolidation services, and has helped thousands of Americans work through debt. Their certified counselors can walk you through your options and help you decide whether a Debt Management Plan or another strategy is right for your situation. It’s a good starting point if you want honest, professional guidance without a sales pitch. Many people leave their first session feeling relieved simply because they finally have a clear picture of their finances.

Credit Counseling vs. Bankruptcy: Which Is Right for You?

Credit counseling works best for people who have a steady income but are struggling to keep up with high-interest debt — particularly credit cards. If your debt is primarily from credit cards and personal loans, and you can afford a reduced monthly payment, a DMP could be a strong alternative to bankruptcy.

Bankruptcy may still be the right option in certain extreme cases — such as when debt is so overwhelming that no realistic payment plan is possible, or when you’re facing serious legal action. But it should always be the last resort, not the first.

A credit counselor can help you honestly assess which category you fall into. That clarity alone is worth the call.

The Sooner You Act, the More Options You Have

One of the biggest mistakes people make is waiting too long to seek help. The longer you go without addressing debt, the fewer options you have. Interest compounds, fees accumulate, and creditors become less willing to negotiate.

Reaching out to a credit counselor early — even before you’ve missed a payment — puts you in the best possible position. It gives you time to explore every option and make a calm, informed decision rather than a desperate one.

Take Control Before Things Get Worse

Debt doesn’t have to define your future. Credit counseling gives you the tools, the plan, and the professional support to tackle it head-on. For the majority of people considering bankruptcy, a better option exists — one that protects your credit, your dignity, and your financial future.

If you’re feeling the pressure of debt right now, don’t wait. Thousands of people in situations just like yours have found a way through with the right guidance. A single conversation with a certified credit counselor could change the direction of your financial life entirely.

{kind=link}