A new EPF withdrawal rule is out, now you can withdraw 90% of EPF balance for buying a house, flat or under construction property. In addition to withdrawal, you can also use EPF fund for repayment of home loan EMI. This new scheme is called as Employee Provident Funds (Fourth Amendment) Scheme 2017. It is applicable from 12th April 2017.

You must be thinking that EPF subscriber was able to withdraw fund for multiple purposes including buying a house, so what’s so new about this? So, let’s take a look at amendment 68 BD recently done by EPFO in the withdrawal rule for buying a house.

Also Read – Online EPF withdrawal Claim Submission Process

EPF withdrawal for buying house and paying EMI

Who can withdraw EPF fund for buying a house?

Following conditions should be satisfied in order to withdraw EPF for buying a house.

- You are a member of a cooperative society or a society registered for housing purpose under any law which is in force and the society has at least 10 EPF members.

- You are ready to purchase a dwelling house or a flat or construction of dwelling house, and

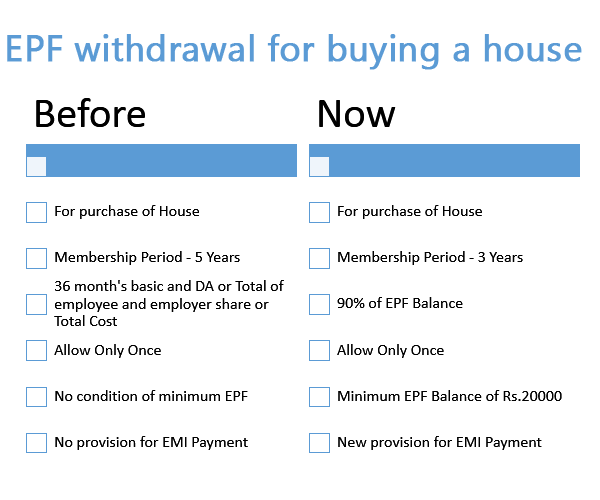

- You are a member of EPF for at least three years. Earlier this limit was five years.

- Your contribution with interest thereon along with the contribution of a spouse who is also a member of EPF must exceed Rs.20000.

- The facility of withdrawal is allowed only once in a lifetime.

For easy understanding comparison between an earlier rule and a new rule is given below in graphical format.

How much amount can be withdrawn?

You can withdraw up to 90% of EPF balance (employee share and contribution of employer including interest) or the construction cost of property whichever is less.

The withdrawal amount shall not be paid to you directly, payment shall be made direct to Cooperative Society or housing agency or builder as the case may be. This amount can be in multiple installments as per authorization from a member.

If the withdrawal amount exceeds the amount required for purchasing a house the extra amount needs to be deposited by EPF subscriber within 30 days of the finalization of the purchase or construction, as the case may be.

Also Read – EPF withdrawal for medical treatment with self-declaration

How to withdraw EPF fund for buying a house?

Step -1 – Member need to apply individually or jointly through housing society in the specific format to the PF Commissioner. The format for applying clearance from PF Commissioner can be download from here.

Step-2 – PF Commissioner needs to issue the certificate that EPF contribution is made by the member or member in last 3 months and the balance as of today, as the case may be. Alternatively, PF member may get a print out of their passbook from the website of EPFO for submitting to the housing society/banks.

Step-3 – Use composite claim form for the withdrawal. If your Aadhaar Number is seeded you can use Aadhaar based EPF Composite Claim Form else you need to use Non Aadhaar Claim form.

How to pay EMI using EPF fund?

Now onwards you can use also use your EPF balance for the repayment of home loan EMI. If you wish to avail this facility you need to instruct EPFO. You can do so by submitting Authorization for repayment of housing loan using PF account.

On receipt of this authorization, EPFO will initiate transfer of EMI Payment to the bank directly as specified by you. EPFO will continue the transfer of this money as long as you maintain sufficient balance in EPF account and your membership is in force.

I hope the information given above will be helpful to you in case you are running out of money for buying a home or for paying EMI.

For more information go through circular published by EPFO on housing scheme.

{kind=link}