Post LTCG many investors started comparing ULIP vs Mutual Fund. I have come across a similar incident where insurance agent has successfully convinced a blog reader, for investing in ULIP by saying LTCG will kill mutual fund returns. In ULIP you enjoy insurance coverage as well as benefit in terms of LTCG exemption. This type of gimmick is always used by an insurance agent or by a banker to trap investors in ULIP.

ULIP is a product designed with the objective of insurance whereas Mutual Fund is pure investment product. However, for understanding let’s take a look at ULIP vs Mutual Fund + Term Plan.

ULIP vs Mutual Fund + Term Plan which one is better?

First, let’s understand the meaning of ULIP, Mutual Fund, and Term Plan. If you are already aware of these products you can skip this section and jump to next section Comparison of ULIP vs Mutual Fund

What is ULIP?

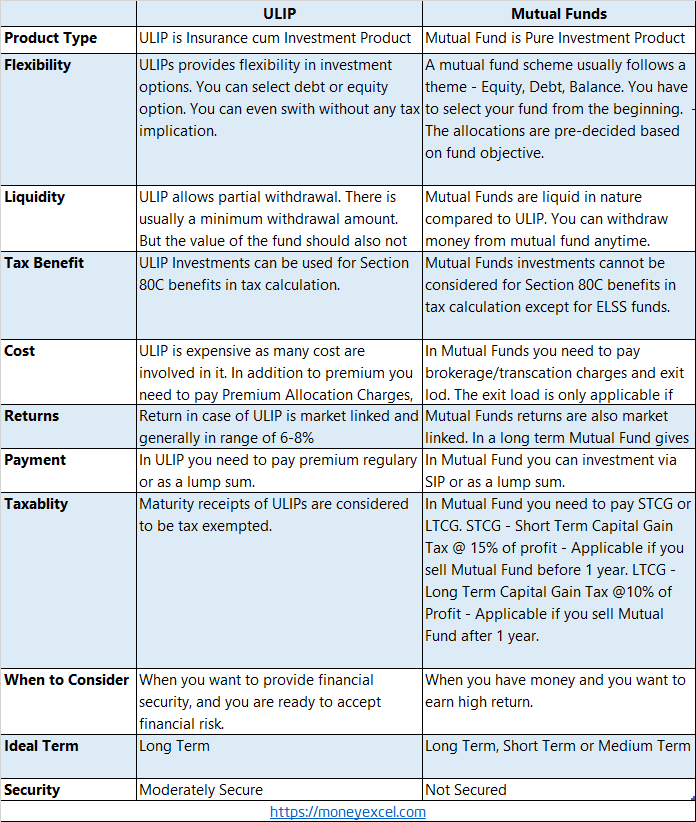

ULIP is Unit Linked Insurance Plan. ULIP is a combination of insurance and investment. This means ULIP holder get the benefit of Insurance as well as investment. A ULIP holder pays premium regularly for insurance. A part of this premium is used for investment.

An Investor can select a type of investment based on risk profile and financial goal. Investment can be either in debt, equity or in both.

Also Read – Top 20 Best Mutual Funds SIP to invest in India for 2018

What is Mutual Fund?

A Mutual Fund is pure investment product. In mutual funds, money collected from investors is used for investment in share, bonds, and other money market instruments. Mutual Funds are professionally managed by experienced fund managers.

What is Term Plan?

A Term plan is a pure insurance product. A term insurance plan provides coverage to the policyholder during the policy term. If the insured expires during policy term then death benefit is payable to the nominee.

Comparison of ULIP vs Mutual Fund

ULIP or Mutual Fund Which One is Better?

Actually speaking, there is no comparison between ULIP and Mutual Fund. Both are different products. ULIP is made for Insurance and Mutual Fund for Investment. One should not mix Insurance with Investment. However, if you are looking for a systematic approach in deciding post-LTCG that you should go for ULIP or Mutual Fund + Term Plan here is a readymade help.

Also Read – Dividend Mutual Funds Equity Scheme – Should You Invest?

First, we will take a look at taxability part especially LTCG. For discussion purpose let’s assume that ULIP and Mutual Fund investments are done for long-term (1 year and above). This clearly means that on Mutual Fund profit you need to pay LTCG @10% above 1 Lakh in a financial year. On the other hand, ULIP maturity amount is tax exempted.

- From taxability point of view, ULIP is a defiantly better choice (post LTCG), provided it offers higher return compared to Mutual Funds.

- ULIP returns are in range of 6-10%. On the other hand, Mutual Fund offers returns in the range of 14-16%. If we apply LTCG also actual return will be higher.

- Another point is – ULIP comes with additional charges which include, Policy administration charges, Premium Allocation Charges, Morality Charges & Fund Management charges. All these charges are deducted from premium before investment. This means actual investment is low. This charges effectively reduce yield by 2-3%. Whereas in Mutual Fund transaction charges are low. If you opt direct mutual fund no transaction fee is applicable.

So, both these products have own advantages and disadvantages. I personally feel that one should give preference to “Direct Mutual Funds” over ULIP.

Over to You –

Don’t get confused, follow a simple method given below.

Go for ULIP –

- When you have low or medium risk appetite.

- When you want life cover along with investment and you are ok with moderate returns.

- When liquidity is not important to you.

- When you want a financial instrument for tax saving.

Go for Mutual Fund –

- When you have a medium or high-risk appetite.

- When you are looking for a pure investment product that offers high returns.

- When you want your investment to be liquid. (Except ELSS).

- When you have term plan to protect your family.

- When you are OK with paying additional LTCG tax.

I hope I have given enough food for thought. If you still have queries related to ULIP or Mutual Fund, just post it in the comment section. I will be more than happy to help you.

{kind=link}