Leave Encashment is a process where you can get money for the unused balance leaves. Most of the people are not aware of Leave Encashment Calculation and Applicable taxes under various conditions. To help them here is complete information about Leave Encashment Calculation and applicable taxes.

Salaried people have different types of leaves like casual leave, privilege leave, sick leave, etc. All these leaves are not encashable. Only a few types of leaves are encashable. One such leave is privilege leave. You can encash privilege leave if it exceeds the specified limit set by the employer.

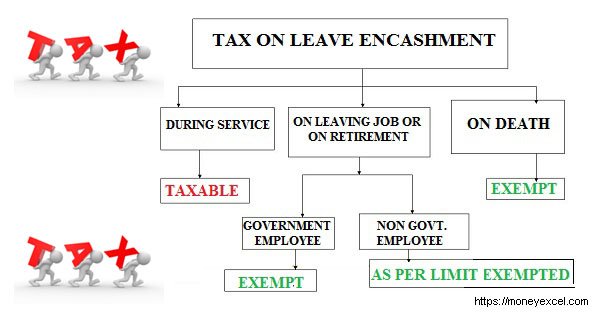

Leave encashment takes place in various conditions like in service, on job change, on retirement, or the death of an employee. Tax applicable on leave encashment varies based on conditions specified above.

Leave Encashment Calculation & Taxes

Leave Encashment

The formula for calculating Leave Encashment is given below. This calculation is for earned leave as per factories act.

- Leave Encashment Amount = (Basic + DA)/26 * No of encashment days)

In the above formula, 26 is the working days of the month. Different companies use different formulas for calculation. The general formula used by most of the companies is given below.

1) 1 day basic salary X No of Earned Leaves

2) (1 day basic salary + 1 day TA + 1 day DA) X No of Earned Leaves

Tax on leave encashment

After looking at the formula of leave encashment let’s look at the applicability of Tax on encashment. The tax applicable on encashment of leave depends upon various factors including time of encashment such as retirement, job change, in service etc. We will take each case separately.

At the time of Retirement

Government Employee

If you are a government employee, the entire amount received as leave encashment is tax-free.

Non-Government Employee:

The leave encashment for private sector employees is specified in section 10 (10AA) and its minimum of following factors.

- Amount received as leave encashment

- Last 10 months average basic salary & dearness allowance before leaving the job

- A maximum cap as stated by the government – Rs 3 Lakhs

We take an example to make the above calculation clear.

Suresh is a private sector employee who receives Rs 5 lakh as his leave encashment at the time of retirement. He worked for 20 years and he was eligible for 35 earned leave per year. Calculation of leave is given below.

- No. Of earned leaves Suresh was eligible for = 35 X 20 = 700 days

- He has taken 340 leaves during the service period.

- Leaves eligible for leave encashment = 700 – 340 = 360 days

- Average last 10 months basic + dearness allowance = Rs 21,000

Tax Calculation

The tax exemption would be minimum of the below 4 points:

- Amount received as leave encashment – Rs 5 Lakhs

- Maximum cap as stated by government – Rs 3 Lakhs

- Last 10 months average basic salary & dearness allowance before leaving the job – Rs 2,10,000 (Rs 21000 X 10)

- Cash equivalent of the leave balance, subject to maximum of 30 days for each completed year of service – Rs 2,87,000 (as per calculation below)

Earned leave eligibility as per above rule = 30 days X 25 = 750 days

Leaves used = 340 days

Leaves eligible for encashment (as per above rule) = 750 – 340 = 410 days (13.5 Months)

Cash equivalent = 13.5 X 21000 = Rs 2,87,000

Tax exemption = Rs 2,87,000

Taxable component = Rs 5,00,000 – Rs 2,87,000 = Rs 2,13,000

At the time of Resignation

For the calculation of leave encashment at the time or resignation, some consider it as a taxable while others prefer to give the same tax treatment at the time of retirement. In the case of the government employee it is tax-free and in the case of non-government employees similar calculation is applicable.

Leave encashment while in Service

Any leave encashment done while in service is fully taxable for both government and non-government employee.

Leave encashment on Death

The leave encashment is tax-free when paid to the nominees or legal heirs at the death of an employee.

Points you should know about Leave encashment

- The calculation of leave encashment is done only for the completed years of services. This means if you have completed 5 years and 10 months of services, the calculation will be done for 5 years only.

- The leave calculation rules are different for different companies. You need to refer to policy and your appointment order for further details.

- Please note that as per rule there is no statutory or legal requirement for employers to offer leave encashment.

- A maximum of 10 months of leave accumulation is allowed to the government employees.

{kind=link}