Let’s be honest — planning for retirement feels overwhelming. You’ve worked hard your whole life, and the last thing you want is to pick the wrong investment and end up short when it matters most. Whether you’re just starting out in your 20s or you’re well into your 40s scrambling to catch up, the question of where to put your money is one that keeps a lot of people up at night.

Two names that keep popping up in every retirement conversation are the National Pension System (NPS) and Mutual Funds. Both are popular, both have their fans, and both promise a better tomorrow. But they’re not the same animal at all — and choosing between them without understanding what’s under the hood could cost you dearly.

So, which one should you pick? Well, that’s exactly what we’re going to dig into today. By the time you’re done reading this, you’ll have a crystal-clear picture of how NPS vs Mutual Funds stack up against each other on the things that matter most: growth potential, tax benefits, and long-term stability. Let’s get into it!

What Exactly Is the NPS?

The National Pension System is a government-backed retirement savings scheme in India, regulated by the Pension Fund Regulatory and Development Authority (PFRDA). It was originally launched for government employees in 2004 and later opened to all Indian citizens in 2009.

Here’s how it works in a nutshell: you contribute money regularly into your NPS account, and that money gets invested across a mix of equities, corporate bonds, and government securities — based on either your own preference or an auto-allocation model based on your age. When you retire (at 60), you can withdraw a portion of the corpus as a lump sum and use the rest to buy an annuity, which pays you a regular monthly income.

Key Features of NPS

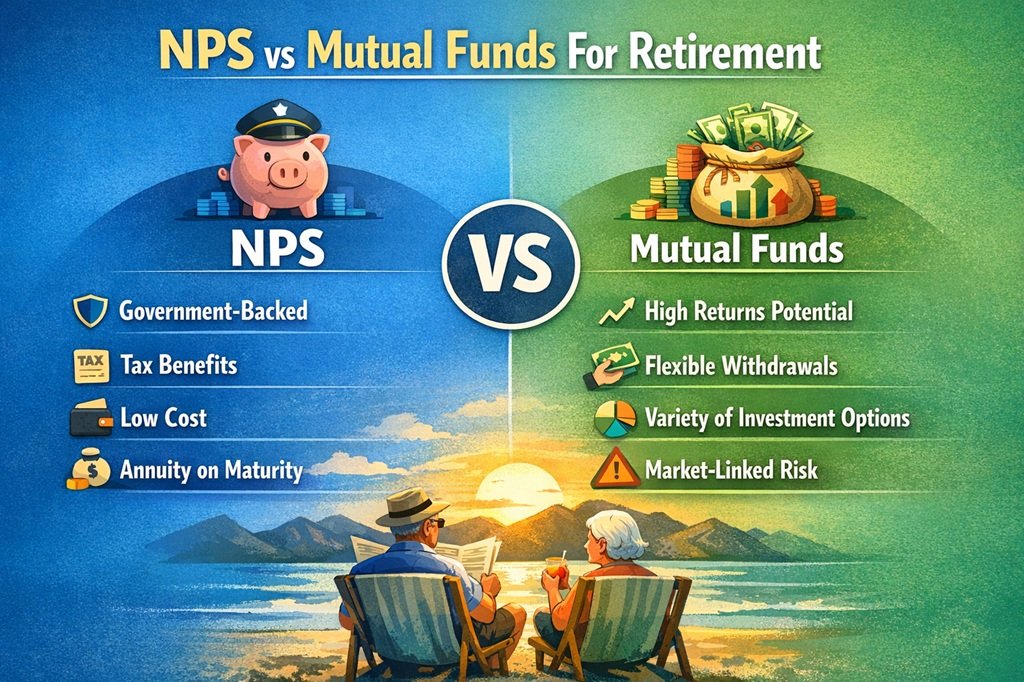

- Regulated by the government — it’s safe and transparent

- Two account types: Tier I (locked-in retirement account) and Tier II (flexible, withdrawal-friendly)

- Low fund management charges — among the lowest in the world

- Market-linked returns with a mix of asset classes

- Mandatory annuity purchase of at least 40% of the corpus at maturity

- Available to Indian citizens aged 18 to 70

It’s got structure, discipline, and government backing — which makes it feel very reassuring. But there are strings attached, and we’ll get to those.

What Are Mutual Funds?

Mutual Funds are pooled investment vehicles where your money gets combined with that of thousands of other investors and managed by professional fund managers. You can invest in equity funds, debt funds, hybrid funds, index funds — the list goes on.

Unlike NPS, mutual funds don’t have a “retirement lock-in” by default. You can start them, stop them, top them up, or even pull your money out whenever you feel like it (subject to exit loads and taxes, of course). That flexibility is both their biggest strength and, for some people, their biggest weakness.

Types of Mutual Funds Relevant for Retirement

- Equity Mutual Funds — High risk, high reward; ideal for long-term wealth building

- Debt Mutual Funds — Safer, steadier; good for capital preservation

- Hybrid/Balanced Funds — A mix of equity and debt

- ELSS (Equity Linked Savings Scheme) — Tax-saving mutual funds with a 3-year lock-in

- Index Funds / ETFs — Low-cost, passive investing options

Now that we know what both options bring to the table, let’s compare them head-to-head.

NPS vs Mutual Funds

When it comes to growing your retirement nest egg, returns matter — a lot. After all, the whole point is to end up with more money than you put in, right?

NPS Returns: What to Expect

NPS returns are market-linked, meaning they’re not fixed. However, historically, the equity component of NPS has delivered returns in the range of 10–12% per annum over the long term. The debt component typically gives around 7–9%. Since NPS blends multiple asset classes, your overall return depends heavily on your asset allocation.

The auto-choice option gradually reduces your equity exposure as you age — which is smart for risk management but may also cap your growth in the final years.

Mutual Fund Returns: What to Expect

Equity mutual funds have historically delivered 12–15% returns annually over long periods (10 years and more). Some well-managed large-cap funds hover around 11–13%, while mid-cap and small-cap funds have surprised investors with even higher returns — though with more volatility.

The thing is, with mutual funds, you’re not locked into any specific allocation. You can go 100% equity when you’re young and gradually shift to debt as you approach retirement. That kind of control can make a significant difference in your final corpus.

Verdict on Growth

When comparing NPS vs Mutual Funds purely on growth potential, mutual funds have the edge — especially if you’re disciplined about asset allocation over time. However, NPS isn’t far behind, and for someone who lacks investment discipline, the forced structure of NPS can actually result in better outcomes.

NPS vs Mutual Funds: Tax Benefits

Ah, taxes. Nobody loves paying them, but everyone loves saving on them. Both NPS and mutual funds offer tax advantages, but they work quite differently.

Tax Benefits Under NPS

NPS is genuinely generous when it comes to tax savings:

- Section 80C — Up to ₹1.5 lakh deduction on NPS Tier I contributions (combined with other 80C investments)

- Section 80CCD(1B) — An additional ₹50,000 deduction exclusive to NPS, over and above the 80C limit. This is a big deal!

- Section 80CCD(2) — If your employer contributes to your NPS, that amount (up to 10% of salary for private employees, 14% for government) is also tax-deductible

- Partial withdrawals — After 3 years, certain withdrawals are tax-free

- At maturity — 60% of the corpus can be withdrawn tax-free; the remaining 40% goes into an annuity (annuity income is taxable)

So essentially, NPS gives you a total potential deduction of up to ₹2 lakh or more per year, which is hard to beat.

Tax Benefits Under Mutual Funds

Mutual funds offer tax efficiency too, but the picture is a bit more nuanced:

- ELSS funds offer up to ₹1.5 lakh deduction under Section 80C, with a 3-year lock-in

- Long-Term Capital Gains (LTCG) on equity funds: gains above ₹1 lakh per year taxed at 10% (after 1 year of holding)

- Short-Term Capital Gains (STCG): taxed at 15% (if sold before 1 year)

- Debt fund gains are now taxed as per your income tax slab (post the 2023 Budget amendment — which was a significant change)

Mutual funds don’t offer any extra deduction the way NPS does with Section 80CCD(1B).

Verdict on Tax Benefits

On the tax front, NPS wins — and it’s not even close. The exclusive ₹50,000 deduction under Section 80CCD(1B) alone gives NPS a meaningful advantage over mutual funds. If you’re in the 30% tax bracket, that’s ₹15,000 saved in taxes every year — just for investing in NPS.

NPS vs Mutual Funds: Stability and Risk Management

Retirement planning isn’t just about chasing the highest returns. It’s about making sure you don’t lose your shirt when markets get rough.

How Stable Is NPS?

NPS is inherently more conservative by design. As you get older, the equity allocation is automatically reduced (under the auto-choice option), and the system pushes you toward more stable debt instruments. This lifecycle approach protects you from a major market crash wiping out your savings right before retirement.

Additionally, NPS invests across equity, corporate bonds, government securities, and alternative assets — so you’re naturally diversified.

The downside? You can’t just exit NPS whenever markets look scary. Your money is locked in, which actually becomes a strength from a behavioral standpoint — it prevents panic-selling.

How Stable Are Mutual Funds?

Mutual funds — especially equity ones — can be wildly volatile in the short term. A market crash can slash your portfolio value by 30–40% overnight. That said, over long periods (10+ years), equity funds have consistently recovered and grown.

The flexibility to withdraw is both a blessing and a curse. Many investors make the mistake of pulling out money during a downturn, locking in losses. Discipline is everything with mutual funds.

For stability-focused investors, debt or balanced mutual funds are much better options, though their growth potential is correspondingly lower.

Verdict on Stability

NPS offers better structural stability thanks to its regulated, diversified, and lifecycle-based approach. Mutual funds can be just as stable if managed well, but they require far more investor discipline and knowledge.

NPS vs Mutual Funds: Flexibility and Liquidity

NPS Liquidity: The Lock-In Reality

NPS Tier I is essentially locked until you turn 60. Yes, there are partial withdrawal options — up to 25% of contributions — but only after 3 years and only for specific reasons like children’s education, home purchase, or medical emergencies. That’s quite restrictive.

The mandatory annuity requirement (at least 40% of corpus must go into an annuity at maturity) is another constraint many investors aren’t thrilled about, since annuity rates in India have historically been quite low.

Mutual Fund Liquidity: Freedom to Move

Mutual funds, on the other hand, are broadly liquid. Most open-ended equity funds can be redeemed within 1–3 business days. There’s no mandatory lock-in (except ELSS), and there’s no rule forcing you to convert your corpus into an annuity.

You can also do Systematic Withdrawal Plans (SWPs) from mutual funds — essentially creating your own monthly “pension” from a lump sum corpus. This gives you both flexibility and income, which is a powerful combination.

Verdict on Flexibility

Mutual funds win, hands down. If life throws curveballs at you — a job loss, a health crisis, a family emergency — having access to your retirement corpus (even partially) is invaluable. NPS’s rigid structure works against you here.

NPS vs Mutual Funds: Charges and Cost Efficiency

NPS Costs

NPS is famous for having some of the lowest fund management charges in the world — typically 0.01% to 0.09% per annum. That’s almost nothing. There are small charges for the Point of Presence (POP) and account maintenance, but overall, the cost structure is very lean.

Mutual Fund Costs

Mutual funds charge an expense ratio ranging from about 0.1% (index funds) to 1.5–2% (actively managed equity funds) per annum. While that might not sound like much, over 20–30 years, the compounding effect of fees can significantly erode your returns.

Verdict on Costs

NPS is far cheaper. If cost minimization is important to you (and it should be!), NPS scores big here.

Who Should Pick NPS and Who Should Pick Mutual Funds?

NPS Is Great For You If…

- You want structured, disciplined retirement savings with a government guarantee

- You’re in a higher tax bracket and want to maximize deductions (especially the ₹50,000 extra under 80CCD(1B))

- You’re a government employee or your employer offers NPS contributions

- You struggle with investment discipline and tend to impulsively withdraw or switch

- You want ultra-low fund management costs

Mutual Funds Are Better For You If…

- You want full control over your money and investment strategy

- You need liquidity and may need to access your corpus before retirement

- You’re comfortable with market volatility and can stay invested long-term

- You want higher growth potential and are willing to accept more risk

- You prefer the flexibility of choosing fund types, managers, and exit timing

Can You Invest in Both? (Spoiler: Yes, You Should!)

Here’s a little secret that most financial advisors will tell you: the best strategy isn’t NPS vs Mutual Funds — it’s NPS and Mutual Funds together!

Use NPS for:

- Disciplined, long-term retirement corpus building

- Maximizing your tax deductions (especially the ₹50,000 extra)

- The stable, low-cost foundation of your retirement plan

Use Mutual Funds for:

- Building additional wealth with higher growth potential

- Maintaining liquidity for pre-retirement emergencies

- Building a flexible income stream through SWPs post-retirement

A combined approach gives you the best of both worlds — NPS handles the “sleep-at-night” portion of your retirement, while mutual funds drive the growth engine.

Frequently Asked Questions (FAQs)

Q1. Is NPS better than mutual funds for long-term retirement planning?

Both have their strengths. NPS offers better tax benefits and structural discipline, while mutual funds offer higher growth potential and flexibility. For most people, a combination of both is the smartest approach.

Q2. Can I withdraw from NPS before retirement?

Yes, but it’s restricted. You can make partial withdrawals (up to 25% of your own contributions) after 3 years, but only for specific reasons like medical emergencies, home purchase, or children’s education.

Q3. Which gives better returns: NPS or mutual funds?

Over the long term, equity mutual funds have historically delivered slightly higher returns (12–15%) compared to the equity component of NPS (10–12%). However, actual returns depend on market conditions and fund selection.

Q4. Is the ₹50,000 NPS deduction worth it?

Absolutely! The additional ₹50,000 deduction under Section 80CCD(1B) is exclusive to NPS and can’t be claimed through any other investment. For someone in the 30% bracket, that’s ₹15,000 saved every year.

Q5. Can NRI invest in NPS?

Yes, Non-Resident Indians (NRIs) are eligible to open an NPS account. However, if they lose their citizenship or become a Person of Indian Origin (PIO), the account must be closed.

Q6. What happens to my mutual fund investment if I need money before retirement?

You can redeem your mutual funds at any point (subject to exit loads if within a year of investment). This is a major advantage over NPS’s locked-in structure.

Q7. Are NPS returns guaranteed?

No, NPS returns are market-linked and not guaranteed. However, the debt portion of NPS (government securities) offers relatively stable returns.

Conclusion

So, who wins the great NPS vs Mutual Funds debate for retirement?

Honestly? Neither wins outright — and that’s the real answer. Both instruments serve different but complementary roles in a well-rounded retirement plan.

If you’re someone who values tax savings, low costs, and forced discipline, NPS is a no-brainer addition to your portfolio. The exclusive ₹50,000 deduction alone justifies using it. On the flip side, if you want growth, flexibility, and the freedom to manage your own wealth journey, mutual funds are your best friend.

The smartest move? Don’t choose between them. Use NPS to lock in your tax benefits and build a disciplined retirement base, and use equity mutual funds to supercharge your wealth over time. That combination is the retirement strategy that actually works — not just in theory, but in the real lives of millions of Indians building their financial future one SIP at a time.

Start early, stay consistent, and don’t let the paralysis of choosing between NPS vs Mutual Funds stop you from investing at all. Because the biggest mistake in retirement planning? Waiting too long to begin.

Your future self will thank you — trust me on that!

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Please consult a certified financial planner before making investment decisions.

{kind=link}