The Central Government has introduced the Unified Pension Scheme (UPS) as an alternative under the National Pension Scheme (NPS) for Central Government staff starting from 1st April 2025. The UPS guarantees payment according to the specified criteria. This scheme aims to provide a stable income post-retirement and ensure financial independence for the elderly. This means that the Unified Pension Scheme is crucial from a retirement planning perspective.

So, how does this scheme work? Who is eligible? What are the benefits? And how can you withdraw your savings? Let’s dive deep into everything you need to know about the Unified Pension Scheme (UPS) in India.

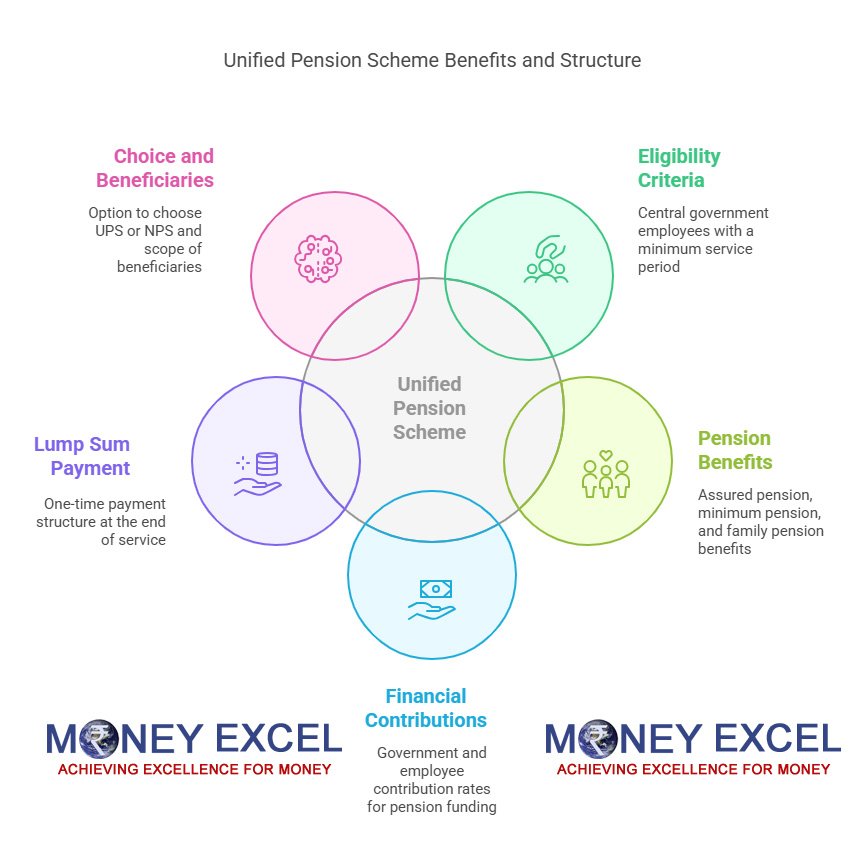

What is the Unified Pension Scheme (UPS)?

The Unified Pension Scheme (UPS) is an initiative by the Indian government to consolidate multiple pension schemes under one umbrella. It ensures that both formal and informal sector workers have access to a structured pension plan. The scheme encourages systematic savings, offering financial security in old age.

At present, government employees are included in the National Pension System (NPS). These employees may either carry on with NPS or transition to the UPS plan. Once employees select UPS, their choice is conclusive and irreversible.

State governments may also embrace and execute the UPS program for employees of the state government. Maharashtra is the inaugural state to adopt UPS.

The objectives of this scheme are given below –

- Provide a single, integrated pension scheme for all working individuals.

- Simplify the pension withdrawal and contribution process.

- Ensure financial stability for retirees.

- Promote long-term savings among Indian citizens.

Unified Pension Scheme (UPS) Eligibility

- A current Central Government employee participating in the NPS and employed as of April 1, 2025.

- A new entrant to the Central Government services, commencing duty on or after 1st April 2025

- An employee of the Central Government who participated in the NPS and has either retired, voluntarily left their position, or retired under the Fundamental Rules 56(j) on or before 31st March 2025.

- The legally married partner of a retired or pensioned Central Government worker who is a subscriber to the NPS and passed away before opting for UPS.

- Self-employed individuals.

- Unorganized sector workers.

- Indian citizens between 18 to 60 years.

UPS Benefits

Guaranteed payouts

- The full guaranteed payout rate will be @50% of the average monthly basic pay over twelve months, effective immediately. A total guaranteed payout is available after at least 25 years of eligibility.

- If the qualifying service period is shorter, a proportional payout would be allowed;

- A guaranteed minimum payout of ₹ 10,000 per month will be guaranteed in the event of retirement. This is after 10 years of qualifying services.

Family Pension

In the event of the payout holder’s death after retirement, the family payout will be 60% of the payout. The payout will be given to the payout holder, immediately before his demise, and will be assured to the legally wedded spouse.

One-Time Payment

A one-time payment will be permitted on superannuation at 10% of monthly earnings (base salary + Dearness Allowance) for each full six months of eligible service. This one-time payment will not influence the amount of guaranteed payout.

Contribution

The corpus under the Unified Pension Scheme option will comprise of two funds, namely –

(a) An individual corpus with employee contribution and matching Central Government contribution; and

(b) A pool corpus with additional Central Government contribution.

The contribution of employees will be 10% of (basic pay + Dearness Allowance). The matching Central Government contribution will also be 10% of (basic pay + Dearness Allowance). Both will be credited to each employee’s individual corpus.

Central Government shall provide an additional contribution of an estimated 8.5% of (basic pay + Dearness Allowance) of all employees who have chosen the Unified Pension Scheme option, to the pool corpus on an aggregate basis. The additional contribution is for supporting assured payouts under the Unified Pension Scheme option.

Investment

The employee can exercise investment choices for the individual corpus alone. Such investment choices shall be regulated by the Pension Fund Regulatory and Development Authority. A ‘default pattern’ of investment may be defined by the Pension Fund Regulatory and Development Authority from time to time. If an employee does not exercise an investment choice on the individual corpus, the ‘default pattern’ of investment will apply.

The investment decisions for the pool corpus built through the additional Central Government contribution will solely rest with the Central Government.

The UPS scheme guarantees a fixed pension sum to government workers after they retire. Employers will add 18.5% of the basic salary plus dearness allowance, while employees will contribute 10% of the basic salary along with dearness allowance each month.

Employees who retire after completing at least 25 years of service will receive 50% of their average basic salary earned in the last 12 months prior to retirement as a pension. For workers who have retired after at least 10 years of service, A pension of ₹10,000 is given monthly after retirement.

How to open NPS account online?

Unified Pension Scheme Gratuity

Retirement Gratuity

Retirement gratuity is the one-time payment given by the employer to the employee upon retirement for working with the company for a designated period. It will be compensated following a minimum of 5 years of employment.

Employees of the central government qualify for retirement gratuity if they meet these conditions:

Superannuation and Invalidation – Retirement takes place when the worker attains the age of 60 or the company’s specified superannuation age. It also occurs when the worker has retired under rule 56 of Fundamental Rules 1922 or rule 12 of the Central Civil Services (Implementation of National Pension System) Rules, 2021.

Distinct Voluntary Retirement Scheme (SVRS) – This program allows government employees deemed excess because of organizational changes to choose early retirement with particular benefits. It promotes workforce efficiency while offering financial assistance to employees who are retiring.

Integration into Other Services – The integration of a government employee into a role within a government-owned or government-funded organization. Upon joining, the employee transitions from the former government role to the new one, carrying over years of service and benefits, subject to certain rules and regulations.

Retirement Gratuity Calculation

Gratuity Amount = (1/4) × Earnings × Completed Six-Monthly Service Periods.

Emoluments = Basic Salary * DA

The gratuity must not go beyond 16.5 times the salary or 25 lakhs, whichever amount is lesser.

Death Gratuity

Death gratuity is a single lump sum payment given to offer financial assistance during a challenging period to the family or nominee of the deceased government worker, irrespective of the duration of their service. The death gratuity is issued if a government employee passes away while in service.

The death gratuity of an employee is determined based on their service tenure.

| Tenure of Service | Death Gratuity |

| < 1 year | 2x emoluments |

| >= 1 year but < 5 years | 6x emoluments |

| >= 5 year but < 11 years | 12x emoluments |

| >= 11 year but < 20 years | 20x emoluments |

| > 20 years | Half of the emoluments for every six months of service |

UPS Withdrawal Guideline

The UPS deductions and calculations of fixed payments for Central Government staff are as follows:

Full Withdrawal upon Retirement – Employees may withdraw as much as 60% of their UPS savings. This withdrawal will, nonetheless, decrease their usual pension payments. If the employee passes away, the spouse will receive 60% of the most recent pension for the duration of their life. Dearness Relief is provided solely to individuals who have begun to receive their pensions.

Partial Withdrawals – Employees are allowed to make partial withdrawals a maximum of three times throughout their employment, after a three-year lock-in duration. Each withdrawal may reach a maximum of 25% of the contributions made by the employee and is permitted under certain conditions, such as:

- Buying or building a house (if the employee does not possess one).

- Supporting children’s education beyond high school or their wedding.

- Addressing healthcare costs associated with long-term conditions or impairments.

- Engaging in personal growth or capacity building.

If an employee is too ill to apply, a relative can start the withdrawal process. Workers can reimburse the sum to maintain their pension advantages unchanged.

FAQs

Whether existing central government employee is eligible to opt for UPS?

Yes, an existing Central Government employee in service as of 1 April 2025, who is covered under the National Pension System (NPS) is eligible to opt for UPS.

What are the timelines to exercise the option of UPS under NPS by an eligible existing (as on 31.03.2025) Central Govt employee?

The option has to be exercised within three (03) months from 1st April 2025, or within such extended timelines if any, allowed by the Central Government.

What happens if the employee fails to opt for UPS within the specified time period?

An eligible person, who does not exercise the UPS option under NPS within the timelines laid down shall be deemed to have opted to continue under NPS without UPS option.

What will happen to my existing corpus on migration from NPS to UPS?

On migration from NPS to UPS, the corpus of the subscriber will get transferred to the PRAN tagged to UPS.

How is the assured payout calculated under UPS?

• The rate of full assured payout will be @50% of 12 monthly average basic pay, immediately prior to superannuation, payable after a minimum 25 years of qualifying service.

• In case of lesser qualifying service period, a proportionate payout would be admissible.

What is the amount of minimum guaranteed payout under UPS?

A minimum guaranteed payout of Rs. 10,000 per month is guaranteed after completing 10 years of service.

Is there any provision for lump-sum payment under UPS?

Yes, a lump-sum amount equivalent to one-tenth of the last drawn basic pay (plus NPA and DA) is paid for every completed 6-month period of qualifying service.

Is there any option to withdraw an amount under UPS at the time of retirement and to what extent?

Yes, UPS Subscriber shall have an option of final withdrawal for an amount not exceeding sixty percent (60%) of the individual corpus or benchmark corpus, whichever is lower, available in the PRAN tagged to UPS as on the date of superannuation or voluntary retirement or retirement, subject to a proportionate reduction in the assured payout payable to such UPS Subscriber.

Can a subscriber make partial withdrawals during the service period?

Yes, partial withdrawals up to 25% of self-contribution (excluding returns) are allowed after completion of lock-in period of three years from the date of enrolment under UPS or NPS whichever is earlier, for specified purposes.

What purposes are allowed for partial withdrawal under UPS?

Higher education of children, marriage of children, purchase/construction of residential house, medical emergencies, disability-related expenses, and skill development.

Conclusion

The Unified Pension Scheme (UPS) India is a robust initiative designed to provide financial stability to retirees. With flexible contributions, government support, tax benefits, and easy withdrawals, it ensures that individuals can secure their future with minimal hassle. If you haven’t yet planned for retirement, now is the time to enroll in UPS and take charge of your financial future.

Retirement planning doesn’t have to be complicated. With the Unified Pension Scheme, you can build a solid foundation for your golden years. So, why wait? Start securing your future today!

– Know the eligibility, benefits, returns, gratuity, and withdrawal rules to plan your future.){kind=link}