P2P lending is now regularized by RBI.P2P lending is easy and fastest way to lend and borrow loans. P2P is also called as peer to peer lending. It is a method of lending money between two individual entities.

Let’s say you are in desperate need of money. It may be due to setting up a new business, marriage, medical emergency or anything else. What do you do? You generally talk to your friend or relative for the money or you approach a bank and take a personal loan – right? Well, what happens if both options do not work for you? P2P lending is alternative to both these options.

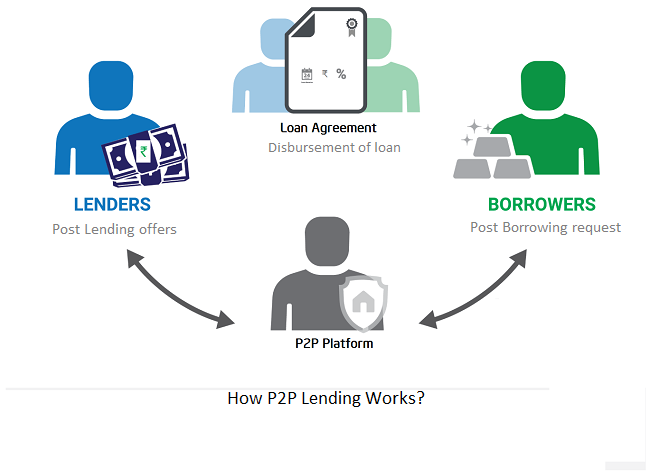

How P2P Lending works?

As discussed in above section for getting a loan from your friends and relative you approach them. To get a loan from the bank you approach the bank. In P2P lending you need to approach P2P lending platform for getting a loan. A P2P platform is a market place like Flipkart and Amazon for getting a loan. You need to follow steps given below on this lending platform.

Step -1 – At first instance, you need to register on the p2p platform as borrower or lender. At the time of registration, you need to provide personal, professional and financial information.

Also Read – Peer to Peer Lending – P2P lending quick and easy way to get loan

Step-2 – P2P platform verifies the trustworthiness of this information by checking proof. This is in line with KYC verification norms.

Step-3- Once verification is completed lender or borrower a can publish their listing on the site mentioning information like the purpose of the loan, interest rate etc.

Step-4 – Borrower or lenders can contact each other. They can also see documentary proof before lending a loan

Step -5 – Loan tenure, a rate of interest and other terms and conditions are discussed between lender and borrower.

Step-6 – On agreement of both lender and borrower disbursement of loan happens. During disbursement, P2P platform plays an important role in making loan agreement and money transfer from lender to the borrower.

There are multiple Peer to Peer lending platforms in India such as Lendbox, Faircent, Peerlend etc.

In order to regulate peer to peer lending platforms, the RBI has issued formal guideline regulating NBFC P2P companies. Take Away from this circular is given below.

- P2P platform needs to register with RBI within 3 months.

- P2P NBFC can neither raise a deposit or nor lend money on its own.

- P2P platforms are not permitted to sell any product except loan specific insurance products.

- NBFC needs to carry out due diligence of participants.

- Limit for lending money is 10 Lakh. Individual lender/investor cannot exceed this limit. This is to ensure that high net worth individual does not become moneylenders by replacing the need for banks.

- The total limit of borrowing money across all P2P is 10 Lakh.

- Fund transfer shall be through Escrow Account mechanism.

- NBFC P2P platform shall make proper agreement disclosing all terms and conditions.

- NBFC P2P needs to make sure that their staff does not harass borrower for recovery of loan.

- NBFC P2P should build robust Information Technology Framework ensuring data security and develop Business continuity plan.

- NBFC P2P needs to submit quarterly statements to RBI.

It is welcome step by RBI to control P2P lending platform. This will surely bring transparency and control to P2P industry. It will also bring trustworthiness to individuals for using this platform.

Do share your views in the comment section.

{kind=link}