– Key Features, Benefits & Review")

LIC Bima Shree Plan 848 is insurance cum money back policy launched by LIC in the year 2018. The tagline for this policy is “Live every moment tension free, buy LIC’s Bima Shree”. This plan is specially designed for High Net worth Investors (HNI) or High-End Customers.

Looking at first instance LIC Bima Shree seems to be a replica of LIC’s Jeevan Shiromani with few changes. Minimum sum assured amount in Bima Shree is changed to 10 Lakh, which was 1 Crore in Jeevan Shiromani. LIC Jeevan Shiromani was providing inbuilt critical illness cover, however new policy LIC Bima Shree is not providing this benefit.

LIC Bima Shree Policy (Plan 848) can be defined as non-linked, with profit, guaranteed additions, limited premium money back plan. Let’s take a quick look at Key features and benefit detail of LIC Bima Shree Plan.

LIC Bima Shree (Plan 848) – Key Features

- Non-Linked, Money Back, Limited Payment, Guaranteed Addition Plan.

- Guaranteed Addition for Full Premium paying term.

- Critical Illness Benefit coverage for fifteen specified critical illnesses available as an optional rider.

- The flexibility of policy term. Policy term can be opted from 14, 16, 18 and 20 years.

- Loan facility after 2 years.

- Money Back in 2 years gap.

- Four Years premium holiday.

- Loyalty Addition after 5 years

- Exclusive Plan for Upper Middle Class

- Survival benefits available for a plan can be deferred, as per the wish of the policy holder.

- Settlement Option for Survival benefits and Claim for 5, 10 and 15 years.

Eligibility for LIC Bima Shree Plan 848

Eligibility conditions for LIC Bima Shree Plan are given in the following table.

| Eligibility for LIC Bima Shree Plan 848 | |

| Minimum Sum Assured | 10 Lakh |

| Maximum Sum Assured | No Limit |

| Policy Term | 14,16,18 and 20 Years |

| Premium Paying Term | Policy Term – 4 Years |

| Minimum Age at Entry | 8 Years |

|

Maximum Age at Entry

|

55 Yrs for 14 Yrs Policy |

| 51 Yrs for 16 Yrs Policy | |

| 48 Yrs for 18 Yrs Policy | |

| 45 Yrs for 20 Yrs Policy | |

|

Maximum Age at Maturity

|

69 Yrs for 14 Yrs Policy |

| 67 Yrs for 16 Yrs Policy | |

| 66 Yrs for 18 Yrs Policy | |

| 65 Yrs for 20 Yrs Policy | |

| Risk Commencement | Immediate |

LIC Bima Shree (Plan 848) – Benefits

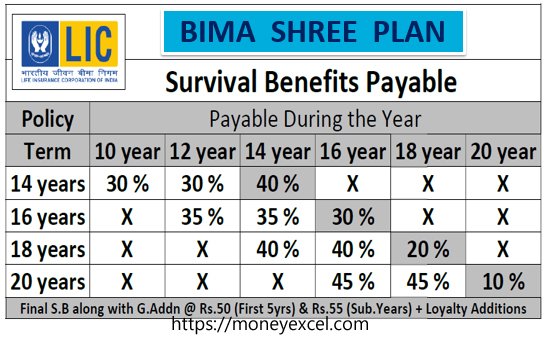

Survival Benefits

If policyholder survives to the specific duration of the policy term, a fixed % of money is payable. The detail of survival benefit is given below –

- For 14 Years Policy – 30% of Basic Sum Assured on 10th and 12th policy year.

- For 16 Years Policy – 35% of Basic Sum Assured on 12th and 14th policy year.

- For 18 Years Policy – 40% of Basic Sum Assured on 14th and 16th policy year.

- For 20 Years Policy – 45% of Basic Sum Assured on 16th and 18th policy year.

Death Benefits

The risk commences under this plan is immediate from the date of issuance of the policy. The death benefit under the plan varies based on the period completed.

- Death occurs during the first 5 years of the plan – 125% of the Basic Sum Assured + Accrued guaranteed additions shall be paid.

- If the death occurs after completion of 5 years – 125 % of Basic Sum Assured + Accrued guaranteed additions + Loyalty additions shall become payable.

Maturity Benefits

On the survival till the maturity term. Following maturity benefit is payable.

- For 14 Years Policy – 40% of Basic Sum Assured + Accrued guaranteed additions + Loyalty additions

- For 16 Years Policy – 30% of Basic Sum Assured + Accrued guaranteed additions + Loyalty additions

- For 18 Years Policy – 20% of Basic Sum Assured + Accrued guaranteed additions + Loyalty additions

- For 20 Years Policy – 10% of Basic Sum Assured + Accrued guaranteed additions + Loyalty additions

For more information refer to the following table –

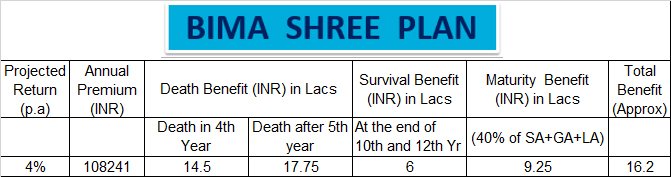

LIC Bima Shree Illustration

In order to understand benefits of this plan let’s take one example. Suppose a person with age 25 plans to buy this policy with a policy term of 14 years and sum assured 10 Lakh. The premium paying term would be 10 years. An annual premium of the policy would be Rs. 108241.

Based on the assumption that projected return by this policy would be 4%, a policy is expected to give following benefits.

The above figures are sample illustration only and are subject to change depending upon loyalty addition declared.

LIC Bima Shree (Plan 848) – Review

Based on the limited information available on LIC Bima Shree Plan 848 I can make out following points-

- LIC Bima Shree seems to be normal Money Back plan by LIC except few changes like money back in shorter duration 2 years and four year premium paying holiday.

- A Guaranteed addition is payable under this plan. However, it will be up to premium paying term only. The value of guaranteed addition is not fixed.

- The Plan is projected as high net worth plan and hence premium of this plan is very high.

- The new change offered by LIC under this plan is loan facility. This plan offers loan facility after 2 years. Generally, all other policies are eligible for a loan after 3 years.

- Critical illness benefits are available as optional benefits under this plan.

- The plan is expected to return 4-6% return as illustrated in the example above.

In short LIC Bima Shree is an old product with a new cover. I suggest to purchase term plan with good coverage and invest remaining amount either in the mutual funds or PPF to earn better returns.