Multibagger Stocks 2024 – Multibagger stocks are stocks that generate returns exceeding 100% (multiple times). Investing in these stocks can result in your investment doubling, tripling, or increasing multiple times. The year 2024 is the year of multibagger stocks. More than 80 stocks have generated more than 100% returns in 2024.

Investors are always attracted to stocks that skyrocket in value and give multifold returns. Many investors are constantly on the lookout for such opportunities. So, in this post, I am here to share with you 45 Multibagger Stocks of 2024. I will also share how you can identify the next big investment opportunity. So, let’s dive into the exciting world of Multibagger Stocks of India 2024!

What Are Multibagger Stocks?

Multibagger is the term discovered by Peter Lynch in his book titled, ‘One Up On Wall Street’. It refers to stocks that grow significantly, typically over 100% of the initial investment. The word Multibagger is a combination of multi and bag. These type of stocks generates multiple times returns and you will need multiple bags to fill up such returns.

A stock that doubles its price is called a two-bagger stock. If stock grows 10 times it is known as 10-bagger stock. If it grows by 100 times it is 100 bagger stock. Multi-bagger stocks are undervalued stocks with strong fundamentals, future business potential, and strong corporate governance.

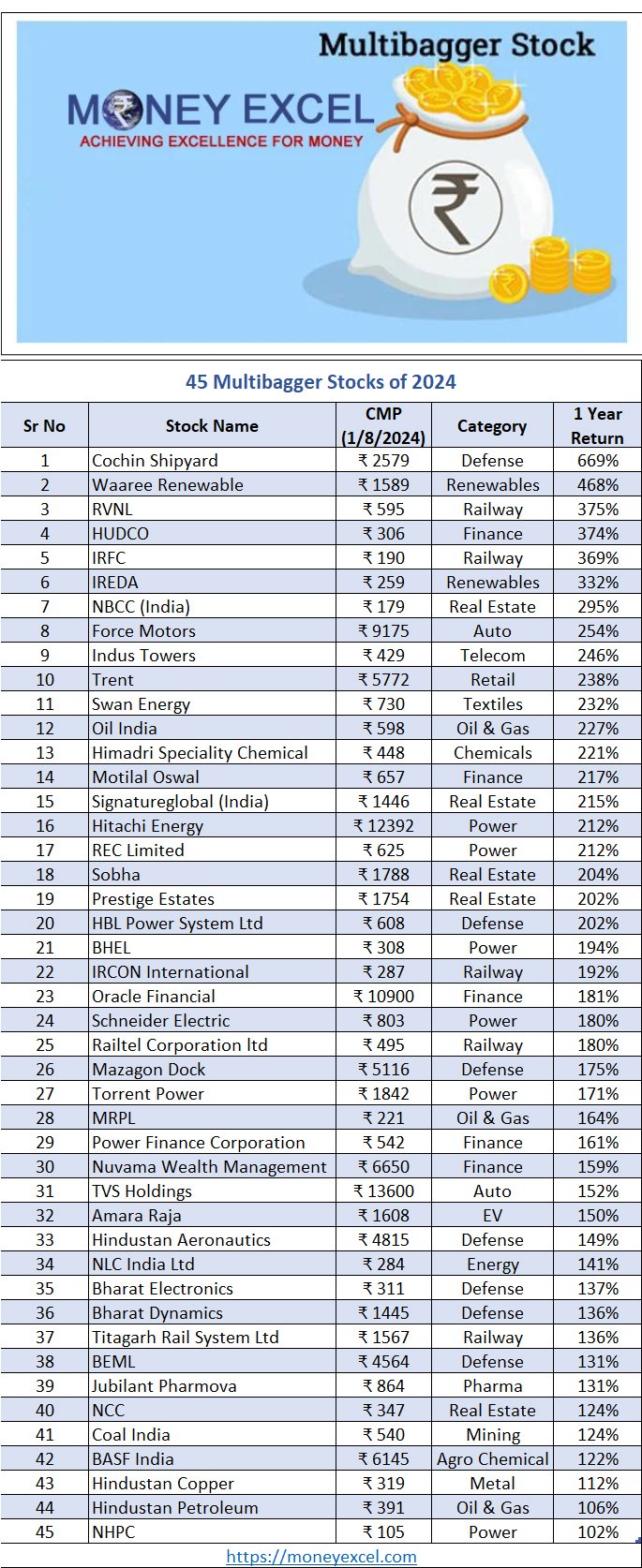

45 Multibagger Stocks of 2024

45 Mutlibagger Stocks of 2024 are Cochin Shipyard, Waaree Renewable, RVNL, HUDCO, IRFC, IREDA, NBCC (India), Force Motors, Indus Towers, Trent, Swan Energy, Oil India, Himadri Speciality Chemical, Motilal Oswal, Signatureglobal (India), Hitachi Energy, REC Limited, Sobha, Prestige Estates, HBL Power System Ltd, BHEL, IRCON International, Oracle Financial, Schneider Electric, Railtel Corporation ltd, Mazagon Dock, Torrent Power, MRPL, Power Finance Corporation, Nuvama Wealth Management, TVS Holdings, Amara Raja, Hindustan Aeronautics, NLC India Ltd, Bharat Electronics, Bharat Dynamics, Titagarh Rail System Ltd, BEML, Jubilant Pharmova, NCC, Coal India, BASF India, Hindustan Copper, Hindustan Petroleum and NHPC. In the last one year from Aug,2023 to Aug, 2024 these stocks have generated more than 100% returns for the investors.

How to find Multibagger Stocks?

Finding the next multibagger requires a keen eye and thorough research. Here are some tips to help you spot these golden opportunities –

Research

Research is extremely important when it comes to finding multibagger stock. You should be capable of doing research and reading financial statements such as profit and loss, asset and liabilities, and revenue statements. You can not find multibagger without doing research. To find such stocks firstly you need to understand the industry dynamics, and growth potential and find out key players.

Analysis of Financial

The next step is to go through the company’s financials. You need to look at the consistent revenue growth, profitability, and low debt levels. A company with strong financial health is more likely to become a multibagger. The business model of the company should be lucrative and sustainable. The product or services of the company must be in demand.

Expansion or New Product Development

Another important factor to consider when making a choice is the expansion or creation of new products. The company needs to always grow its business or innovate new products. An instance of this is Patanjali. Patanjali is consistently growing the company and introducing new products to expand its customer base.

Strong Management Team

Companies led by visionary leaders tend to outperform. You should evaluate the management team’s track record. Management should be capable of making appropriate decisions in response to a dynamic business environment. Similar to adopting new products, technology, or pivoting business strategies. Transparency in management and adherence to corporate governance standards are crucial.

Favorable Market Conditions

Identify what sets the company apart from its competitors. Whether it’s a unique product, superior technology, or a strong brand, a competitive edge is crucial for long-term growth.

Market Trend

You should stay updated with market trends and news. Understanding macroeconomic factors, government policies, and global events can provide insights into potential growth areas. For example, currently, the government is focusing on electric vehicles and defense. This means stocks for these sectors are likely to perform well.

Common Mistakes to Avoid

Many investors make common mistakes while selecting and investing in such stocks and end up making losses. You should avoid some common mistakes here are the details.

Never Ignore Fundamentals

Fundamentals are basics. Stick to the basics. Don’t invest in a stock solely based on market trends or recommendations. Thoroughly analyze the company’s fundamentals before making a decision.

Valuation

Valuation is extremely important while investing in stocks. Don’t get caught up in the hype. Ensure you’re not overpaying for a stock by analyzing its price-to-earnings ratio, price-to-book ratio, and other valuation metrics.

Performance History

You should not invest in a stock based on performance history. A stock that has given multibagger returns in the past does not mean it will give similar returns in the future.

Diversification

You should avoid putting all your eggs in one basket. Diversify your portfolio across different sectors and stocks to mitigate risks.

FAQs

What are multibagger stocks?

Multibagger stocks are stocks that yield returns exceeding 100% of the initial investment, often multiplying the original amount.

Why is India a good market for multibagger stocks in 2024?

India’s favorable economic reforms, digital revolution, and infrastructure development make it an attractive market for businesses, offering the potential for multibagger stocks.

How can I identify potential multibagger stocks?

Conduct industry research, assess financial statements, judge management performance, pinpoint competitive strengths, and stay informed about market trends.

What pitfalls should I avoid when investing in multibagger stocks?

Avoid overvaluation, lack of diversification, and ignoring fundamentals.

Conclusion

Investing in multibagger stocks of India in 2024 has the potential to help you build significant wealth. By pinpointing businesses with promising growth prospects, solid financial well-being, and competitive advantage, you can greatly improve your investment portfolio. Do not forget that conducting thorough research and making informed decisions are essential for successful investing. Be alert, stay informed about market trends, and prepare to capitalize on the next major investment opportunity!