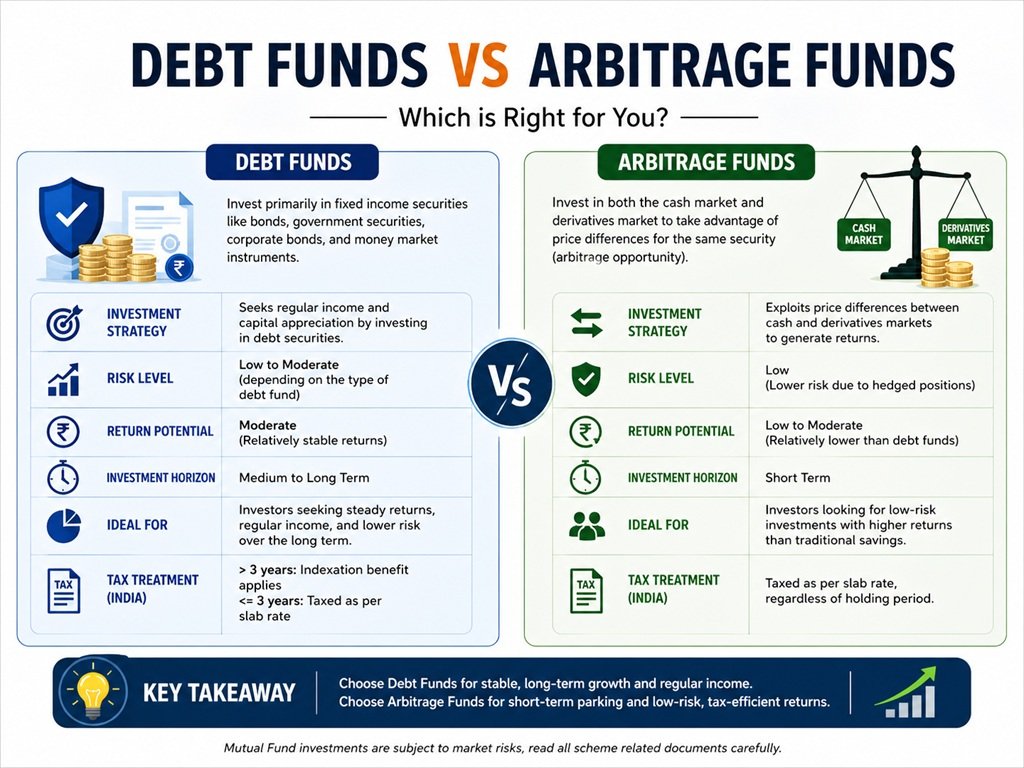

When you have money sitting idle for a short period — maybe you are saving up for a goal three months away, waiting to deploy funds into equity at the right time, or just want your emergency corpus to earn something decent — simply leaving it in a savings account feels like a missed opportunity. Two mutual fund categories come up consistently in this conversation: arbitrage funds and Debt Funds.

Both are considered low-risk. Both are short-term friendly. Both are widely used by individual investors and large corporations alike for parking surplus cash. But they work in fundamentally different ways, carry different risk profiles, have different tax treatments, and suit different types of investors.

This article covers everything you need to understand about both types of funds, including how each one works, what you can realistically expect in terms of returns and costs, the tax treatment under current rules, their limitations, and a clear guide on which one makes more sense for your specific situation.

What Are Arbitrage Funds?

Arbitrage funds are hybrid mutual funds that exploit price differences between two markets for the same underlying asset. The most common form is simultaneous buying in the cash (or spot) market and selling in the futures market, locking in the price gap as profit.

SEBI mandates that arbitrage funds maintain at least 65% of their total assets in equities or equity-related instruments. This classification is crucial — it means arbitrage funds are taxed like equity funds, which has important benefits for certain investors, as we will discuss later.

How the Arbitrage Strategy Actually Works

Let us walk through a concrete example to make this very clear.

Spot market: Shares of Company ABC are trading at ₹500 per share.

Futures market: The one-month futures contract for ABC is trading at ₹510 per share.

The arbitrage fund simultaneously buys 1,000 shares at ₹500 in the spot market and enters a futures contract to sell 1,000 shares at ₹510. The profit of ₹10 per share (₹10,000 total) is locked in at the moment of entering both trades. On expiry of the futures contract, both positions are settled, the ₹10 spread is captured, and the fund moves on to the next opportunity.

The beauty of this strategy is that it is market-neutral. The fund does not care whether the price of ABC goes up or down by the time the futures contract expires. The profit is the spread, not the market direction. This is why arbitrage funds maintain very low correlation with overall equity market movements.

However, the fund must continuously find fresh arbitrage opportunities. After one futures contract expires, the manager must identify and enter new trades. The availability of these opportunities depends heavily on how volatile the market is.

What Happens When Arbitrage Opportunities Are Scarce?

When market volatility is low, the gap between the spot price and futures price narrows. There is simply less spread to capture. During quiet market periods, the arbitrage fund’s returns can compress significantly — sometimes to levels comparable to or even slightly below Debt Funds.

To handle this, arbitrage funds typically park the non-equity portion (up to 35% of assets) in debt instruments like treasury bills, certificates of deposit, and high-quality short-term bonds. This acts as a buffer, providing some baseline returns even when pure arbitrage opportunities are thin.

Key Point: Arbitrage funds are classified as equity funds by SEBI, taxed like equity, but carry very low market risk because positions are always fully hedged.

Advantages of Arbitrage Funds

- Market-neutral and low risk: Since every buy position is offset by a corresponding sell in futures, the fund is not exposed to directional market movements. A stock market crash does not hurt an arbitrage fund the way it hurts a pure equity fund.

- Equity taxation on a debt-like risk profile: This is the defining feature. The 65% equity exposure qualifies them for equity fund tax treatment. After one year, gains attract long-term capital gains tax of 12.5% (above ₹1 lakh). This is far lower than the income slab tax on liquid fund gains for high-income investors.

- Relatively stable returns in moderate-to-high volatility markets: When market volatility is healthy, these funds can consistently earn 5.5% to 7.5% annualised, sometimes more.

- No credit risk on the equity portion: The fund buys the actual shares, so it does not depend on any company’s ability to repay debt — unlike the debt portion of Debt Funds.

- Useful for corporates and HNIs: Companies and high-net-worth individuals in the 30% tax bracket find arbitrage funds significantly more tax-efficient for parking surplus funds beyond 30 days.

Disadvantages of Arbitrage Funds

- Exit load if redeemed before 30 days: Most arbitrage funds charge a 0.25% to 0.50% exit load on redemptions within 30 days. This makes them less suitable for very short holding periods — say, one to two weeks.

- Redemption takes 2 to 3 business days (T+2 or T+3): Unlike Debt Funds which process redemptions on T+1, arbitrage funds take two to three days. In a genuine emergency, this delay can be inconvenient.

- Returns depend on market volatility: In prolonged low-volatility market phases, arbitrage opportunities dry up and returns compress. There is no guarantee of any specific minimum return.

- Higher expense ratio than Debt Funds: Active management of arbitrage positions and higher transaction costs push up the expense ratio, which reduces the net return to investors.

- Not a fixed-return instrument: Returns fluctuate based on futures market conditions and spread availability. Past returns are not a reliable guide to near-term returns.

What Are Debt Funds?

Debt Funds are debt mutual funds that invest exclusively in short-term money market instruments. As per SEBI regulations, Debt Funds can only invest in securities with a residual maturity of 91 days or less.

The instruments they typically invest in include treasury bills (T-bills issued by the government), certificates of deposit (CDs issued by banks), commercial papers (CPs issued by companies), and collateralised borrowing and lending obligations (CBLOs). All of these are either government-backed or issued by highly rated entities, which is why the credit risk in Debt Funds is generally very low.

Because the portfolio consists of very short-maturity instruments, Debt Funds are largely immune to interest rate movements. If interest rates rise, existing bond prices fall — but instruments that mature in 30 to 90 days have almost no price sensitivity to rate changes.

How Debt Funds Generate Returns

Debt Funds earn returns primarily through the interest income generated by the instruments they hold. When the fund buys a 60-day commercial paper at a discount to its face value, the difference between the purchase price and the face value (the interest) accrues daily in the fund’s NAV. This is why liquid fund NAVs typically move upward in a very steady, almost linear fashion — there are no big jumps up or down.

On most business days, the NAV of a liquid fund increases by a small, predictable amount. This gives investors the feeling of a very stable investment, which is exactly why corporates and treasuries use Debt Funds to park working capital.

Did You Know: Debt Funds are one of the few mutual fund categories where the NAV is published for all 7 days of the week, including weekends, to reflect the daily interest accrual.

Advantages of Debt Funds

- Fastest redemption in the mutual fund universe: Debt Funds support T+1 redemption — meaning if you redeem today, the money reaches your bank account on the next business day. Most platforms also support instant redemption of up to ₹50,000 or 90% of the portfolio value, whichever is lower.

- No exit load for redemptions after 7 days: Debt Funds have an exit load of 0.0070% on day 1, reducing to nearly zero by day 7, and zero thereafter. There is no minimum holding period to avoid penalties — unlike arbitrage funds which impose exit loads for 30 days.

- Very low risk: Investing only in high-quality, short-maturity debt instruments means the probability of loss in a liquid fund is extremely low under normal market conditions.

- Highly predictable returns: Liquid fund returns are stable and consistent, typically in the 5.5% to 7% annualised range, with very little day-to-day variation. This predictability makes financial planning much easier.

- No lock-in period: You can invest and redeem at any time without any mandatory holding period or restriction (beyond the 7-day exit load window).

- Beats savings accounts for idle cash: Most savings accounts offer 2.5% to 3.5% per year. Even after taxes, Debt Funds often outperform savings accounts for money parked for a month or more.

Disadvantages of Debt Funds

- Gains are taxed as per income slab: Liquid fund returns, whether held short or long term (under 3 years), are added to your income and taxed at your applicable slab rate. For someone in the 30% bracket, this significantly erodes post-tax returns.

- Not completely risk-free: While very rare, Debt Funds can experience losses. In 2019, several Debt Funds suffered NAV drops due to exposure to IL&FS group securities, which defaulted. SEBI has since tightened norms, but some residual credit risk remains.

- Interest rate sensitivity: Though minimal, Debt Funds are not entirely immune to interest rate changes. A sudden, sharp rise in short-term rates can cause temporary NAV fluctuations.

- Lower returns in a falling interest rate environment: When the RBI cuts interest rates, the yields on money market instruments fall, and liquid fund returns reduce accordingly.

Arbitrage Funds vs Debt Funds: Detailed Comparison

| Aspect | Arbitrage Funds | Debt Funds |

| SEBI Classification | Hybrid Fund | Debt Fund |

| Primary Strategy | Buy in spot market, sell in futures market (fully hedged) | Invest in short-term money market instruments (91-day max maturity) |

| Equity Exposure | Minimum 65% in equities/equity derivatives | Zero — 100% debt instruments |

| Risk Level | Low (market-neutral), but some return variability | Very low — consistent and stable |

| Redemption Speed | T+2 to T+3 business days | T+1; instant redemption available up to ₹50,000 |

| Exit Load | ~0.25%-0.50% if redeemed within 30 days | Graded exit load for first 7 days; zero after 7 days |

| Return Potential | 5.5%-7.5%+ annualised (varies with volatility) | 5.5%-7% annualised (relatively stable) |

| Return Consistency | Varies with market volatility conditions | Highly consistent and predictable |

| Taxation (Short-term) | 20% if held less than 1 year | As per income tax slab rate |

| Taxation (Long-term) | 12.5% after 1 year (above ₹1 lakh gain) | As per income tax slab rate if held under 3 years; 12.5% after 3 years |

| Best For | Investors in 30%+ tax bracket, 1-month+ horizon | Conservative investors, emergency funds, very short-term parking (1-7 days) |

| Market Dependency | Dependent on market volatility for returns | Largely independent of equity markets |

| Expense Ratio | Moderate to high (0.30%-0.80%) | Low (0.05%-0.20%) |

| Ideal Holding Period | 1 month to 1+ year | 1 day to 3 months |

Understanding Returns: A Realistic Comparison

What Returns Can You Actually Expect?

Returns from both fund types are not guaranteed and change based on market conditions and the interest rate environment. That said, here is a realistic range to anchor your expectations.

Arbitrage funds have historically delivered returns in the 5.5% to 7.5% annualised range over a medium-term holding period. When market volatility is high — during earnings seasons, major policy announcements, or global events — the futures spreads widen and arbitrage returns increase. During dull, low-volatility phases, returns can drop to 5% or even lower.

Debt Funds have historically returned between 5.5% and 7% annualised, with returns closely tracking prevailing short-term interest rates in the economy. When the RBI is in a rate-cutting cycle, liquid fund returns fall. When rates are high or stable, returns are better.

Post-Tax Returns: The Real Difference

The raw returns of both fund types look similar. The meaningful difference appears after taxes, particularly for investors in higher tax brackets. Consider this comparison:

| Scenario | Arbitrage Fund | Liquid Fund |

| Holding Period | 1 year+ | 1 year+ |

| Pre-tax Returns (assumed) | 7% p.a. | 7% p.a. |

| Tax Rate (30% bracket investor) | 12.5% LTCG after 1 year | 30% slab rate |

| Tax on ₹7,000 gain | ₹875 (12.5%) | ₹2,100 (30%) |

| Post-tax return | ~6.1% effective | ~4.9% effective |

| Advantage | Arbitrage fund wins by ~1.2% | — |

This difference of around 1 to 1.5 percentage points in post-tax returns might seem small, but on a corpus of ₹25 to 50 lakhs parked for a year or more, it translates to a meaningful sum. This is why high-income professionals, business owners, and HNIs strongly prefer arbitrage funds for their surplus funds.

However, the equation reverses for short holding periods. If you plan to park money for just 1 to 3 weeks, arbitrage funds impose an exit load (effectively wiping out much of the return), and the tax advantage of equity classification only kicks in after one year. For very short durations, Debt Funds are both simpler and more cost-effective.

Taxation: A Detailed Look

Taxation on Arbitrage Fund Gains

Since SEBI classifies arbitrage funds as equity-oriented funds (due to the 65% minimum equity exposure), they are taxed under the equity fund rules.

- Short-term capital gains (STCG): If you sell your arbitrage fund units within 12 months of purchase, the gains are treated as short-term capital gains and taxed at a flat rate of 20% (as of the 2024 Budget update, increased from the earlier 15%).

- Long-term capital gains (LTCG): If you hold for more than 12 months, gains are classified as long-term and taxed at 12.5% on amounts exceeding ₹1 lakh per financial year. Gains up to ₹1 lakh per year are completely tax-free.

Taxation on Liquid Fund Gains

Debt Funds are debt funds, and their taxation follows debt fund rules under the post-April 2023 framework (which removed the indexation benefit on new debt fund investments).

- All capital gains taxed at slab rate: Regardless of how long you hold a liquid fund — whether 30 days or 3 years — the gains are added to your total income and taxed at your applicable income tax slab rate.

- Long-term holding provides no tax advantage: Unlike the old rules where holding debt funds for 3 years gave you indexation benefits, the new rules (applicable for funds purchased from 1 April 2023) offer no such benefit. Everything is taxed at slab rates.

Who Benefits from Which Tax Treatment?

| Investor Profile | Better Option (Post-Tax) | Reason |

| Investor in 30% tax bracket, 1+ year horizon | Arbitrage Fund | 12.5% LTCG vs 30% slab — saves ~17.5% |

| Investor in 20% tax bracket, 1+ year horizon | Arbitrage Fund | 12.5% LTCG vs 20% slab — saves ~7.5% |

| Investor in 5% or zero tax bracket | Liquid Fund | Minimal tax anyway; no exit load advantage needed |

| Any investor, holding <30 days | Liquid Fund | Arbitrage exit load kills the return advantage |

| Any investor, holding 30 days to 1 year | Context-dependent | Compare post-tax returns based on actual slab rate |

| Corporate treasury, any duration 1+ month | Arbitrage Fund | High tax bracket, significant tax savings |

Liquid Fund Liquidity

The name says it all. Debt Funds are designed to be the most accessible category of mutual funds. The standard redemption timeline is T+1, meaning you get your money the next business day. However, in recent years, most major platforms have introduced instant redemption for Debt Funds.

Under SEBI’s instant redemption facility, you can withdraw up to ₹50,000 or 90% of the current value of your investment (whichever is lower) instantly, with the amount hitting your bank account within minutes. This makes Debt Funds a genuine alternative to a savings account for emergency funds.

There is a graded exit load for the first seven days: 0.0070% on day 1, 0.0065% on day 2, scaling down to 0.0010% on day 6, and zero from day 7 onwards. In practical terms, this is so small that it is unlikely to deter any investor.

Arbitrage Fund Liquidity

Arbitrage funds are reasonably liquid but not in the same league as Debt Funds. Standard redemption takes two to three business days (T+2 or T+3), which is the same as most equity funds. This is because executing the position — settling the equity holding and closing the futures position — takes time.

There is also the exit load consideration: most arbitrage funds charge 0.25% to 0.50% if you redeem within 30 days. This makes them effectively illiquid for very short-term needs. If you might need the money within two to three weeks, an arbitrage fund is not the right choice.

However, for money you are comfortable keeping invested for a minimum of one month — ideally three months or more — the T+2 redemption timeline is unlikely to be a major inconvenience.

Practical Rule: Keep your emergency fund in Debt Funds (or overnight funds). Park money you won’t touch for 1+ months in arbitrage funds if you are in a high tax bracket.

Risks in Arbitrage Funds

The primary risk in an arbitrage fund is not market risk — since positions are hedged — but execution risk. If there is a lag between buying in the spot market and selling in the futures market, or if the spread compresses unexpectedly, the fund may earn less than anticipated.

There is also the risk of futures contracts being illiquid for certain stocks, which forces the fund to work with fewer or lower-quality arbitrage opportunities. Additionally, if corporate actions (like mergers, demergers, or bonus issues) affect a stock held in the arbitrage portfolio, managing the position becomes complex.

Counterparty risk is another factor. The futures exchange acts as the counterparty, which significantly reduces (but does not eliminate) default risk.

Risks in Debt Funds

Debt Funds are very safe, but not risk-free. The main risks are:

- Credit risk: If a company that issued commercial paper defaults, the liquid fund holding that paper will take a hit. SEBI’s current rules restrict Debt Funds from investing in lower-rated instruments, which significantly reduces this risk.

- Interest rate risk: Very minimal due to the 91-day maturity cap, but not zero. A sudden sharp rise in short-term rates can cause brief NAV discomfort.

- Concentration risk: If the fund is heavily exposed to one sector or issuer and that issuer faces trouble, the impact can be sharp. SEBI limits per-issuer exposure, but diversification quality still varies across fund houses.

Costs: Expense Ratio and Transaction Charges

Every mutual fund deducts an annual expense ratio from the fund’s assets to cover management and operational costs. This cost directly reduces the investor’s returns.

Debt Funds have among the lowest expense ratios in the mutual fund industry — typically between 0.05% and 0.20% per year for direct plans. Since the investment strategy is straightforward (buying and holding short-maturity debt instruments), there is little need for expensive active management.

Arbitrage funds have noticeably higher expense ratios, generally between 0.30% and 0.80% per year for direct plans. This is because the arbitrage strategy involves continuous trading — buying and selling in both spot and futures markets repeatedly as each futures contract expires. Each trade involves brokerage and impact costs that add up.

The higher expense ratio of arbitrage funds is an important consideration. If two funds generate the same gross return, the one with the lower expense ratio puts more money in your pocket. The tax advantage of arbitrage funds typically more than offsets the higher costs for investors in high tax brackets — but for investors in lower tax brackets, the numbers may not work in arbitrage funds’ favour.

Which Fund Is Right for You?

Choose a Liquid Fund If:

- You need access to your money within 1 to 7 days with no penalties.

- You are building or maintaining an emergency fund and need instant access.

- You are in a lower income tax bracket (5% or zero) and the tax treatment difference is minimal.

- You are parking money for a very short period — less than one month — and want to avoid exit loads entirely.

- You are an institution or treasury looking for same-day or next-day liquidity with stable NAV.

- You are a first-time investor uncomfortable with any equity-linked product label, even if the actual risk is low.

Choose an Arbitrage Fund If:

- You are in the 20% or 30% income tax bracket and want to reduce your tax burden on short-term parked funds.

- You can commit to keeping the money invested for at least 30 to 90 days to avoid exit loads.

- You are looking to hold for one year or more to access the 12.5% LTCG tax rate.

- You are a corporate or HNI looking to park significant sums (₹10 lakh+) tax-efficiently.

- You understand that returns may vary with market volatility and are comfortable with that variability.

- You are looking for a relatively stable parking option with tax efficiency and can tolerate T+2 to T+3 redemption.

A Practical Decision Guide

| Your Situation | Recommended Fund |

| Emergency fund — need money anytime, instantly | Liquid Fund |

| Parking salary for 2-3 weeks before next investment | Liquid Fund |

| HNI, 30% tax bracket, 3-month surplus | Arbitrage Fund |

| Corporate treasury with 1-month surplus | Arbitrage Fund |

| Conservative retiree, capital safety paramount | Liquid Fund |

| Young investor, 1+ year horizon, moderate tax bracket | Arbitrage Fund |

| Anyone needing money in under 30 days | Liquid Fund |

| Anyone wanting 12.5% LTCG treatment on parked funds | Arbitrage Fund (hold 1+ year) |

Some Well-Known Funds in Each Category

While this article does not recommend specific funds, it is helpful to know which fund houses are active in each category. Always check current ratings, recent performance, expense ratios, and AUM before investing.

Established Arbitrage Fund Options

- HDFC Arbitrage Fund

- Nippon India Arbitrage Fund

- ICICI Prudential Equity Arbitrage Fund

- SBI Arbitrage Opportunities Fund

- Kotak Equity Arbitrage Fund

These funds have been around long enough to be evaluated across different market volatility cycles.

Established Liquid Fund Options

- Parag Parikh Liquid Fund

- HDFC Liquid Fund

- Axis Liquid Fund

- ICICI Prudential Liquid Fund

- SBI Liquid Fund

When evaluating Debt Funds, pay particular attention to the credit quality of the portfolio — ensure the fund invests primarily in AAA-rated instruments and government securities.

Conclusion

Arbitrage funds and Debt Funds occupy similar spaces in the short-term investment landscape, but they are not interchangeable. The right choice depends on three main factors: how long you can stay invested, how quickly you might need the money, and what income tax bracket you are in.

Debt Funds are the go-to choice for emergency corpus management, very short-term parking (under 30 days), and conservative investors who prioritise stability and instant access above all else. They are simple, reliable, and offer the best liquidity in the mutual fund space.

Arbitrage funds are the better choice for investors who can commit to at least 30 days — and ideally one year or more — and who are in higher tax brackets. The equity tax classification is a genuine and significant advantage that compounds meaningfully over time. Corporate treasuries and HNIs particularly benefit from this structure.

Neither fund type is universally superior. Evaluate your own holding period, tax situation, and liquidity needs honestly, and pick the one that aligns best with your goals. Many savvy investors use both — Debt Funds for their emergency buffer and arbitrage funds for their medium-term surplus.

Frequently Asked Questions

1. Is it safe to invest in arbitrage funds?

Yes, arbitrage funds are generally safe because every equity position is fully hedged with an opposite futures position. The fund has very low directional market risk. However, returns are variable and depend on market conditions. They are not guaranteed.

2. Can I lose money in a liquid fund?

Liquid fund losses are extremely rare but not impossible. If a portfolio holding defaults (as happened with IL&FS-linked securities in 2018), the fund’s NAV can drop. SEBI has tightened norms since then. Always check the credit quality of the fund’s portfolio before investing.

3. What is the minimum investment in arbitrage and Debt Funds?

Most funds accept a minimum investment of ₹500 to ₹1,000 for lump sum purchases and ₹500 for SIPs. Check the specific fund’s scheme information document for exact minimums.

4. Are arbitrage funds better than fixed deposits for short-term parking?

For investors in the 30% tax bracket, arbitrage funds held for one year or more often outperform FDs on a post-tax basis, since FD interest is taxed at the full slab rate. However, FDs offer a guaranteed return and zero market-related variability, which arbitrage funds do not.

5. Do arbitrage funds have SEBI’s instant redemption facility?

No. Instant redemption is a feature specific to Debt Funds and overnight funds. Arbitrage fund redemptions follow the standard T+2 to T+3 process.

6. How do interest rate changes affect these funds?

Debt Funds are directly affected by short-term interest rate changes — when rates rise, liquid fund returns improve; when rates fall, returns decrease. Arbitrage funds are largely insulated from interest rate changes on the equity portion, though the debt portion (up to 35%) does have some sensitivity.

7. Can NRIs invest in arbitrage and Debt Funds?

Yes, NRIs can invest in both through NRE or NRO accounts. However, tax treatment may differ based on residency status and the applicable Double Taxation Avoidance Agreement between India and the NRI’s country of residence. Consult a tax advisor before investing.

{kind=link}