In the world of investing, things can sometimes feel complicated. There are so many choices out there, like stocks, bonds, and mutual funds. But what if there was a way to make saving for big life goals easier? That’s where the Securities and Exchange Board of India, or SEBI, comes in. SEBI is the main regulator for India’s stock markets and investment products. They make rules to protect investors and keep things fair. Recently, on February 27, 2026, SEBI announced a brand-new type of mutual fund called Life Cycle Funds. These are designed to help people invest based on their specific goals, like saving for retirement or a child’s education.

Let me break this down step by step. Mutual funds are basically pools of money from many people, managed by experts who invest it in different things to grow it over time. The old way had something called solution-oriented funds, which were meant for things like retirement or kids’ futures. But SEBI decided to scrap those and replace them with these new Life Cycle Funds. Why? Because they think this new setup will make investing smarter and less stressful for everyday people.

What Are Life Cycle Funds and Why Do They Matter?

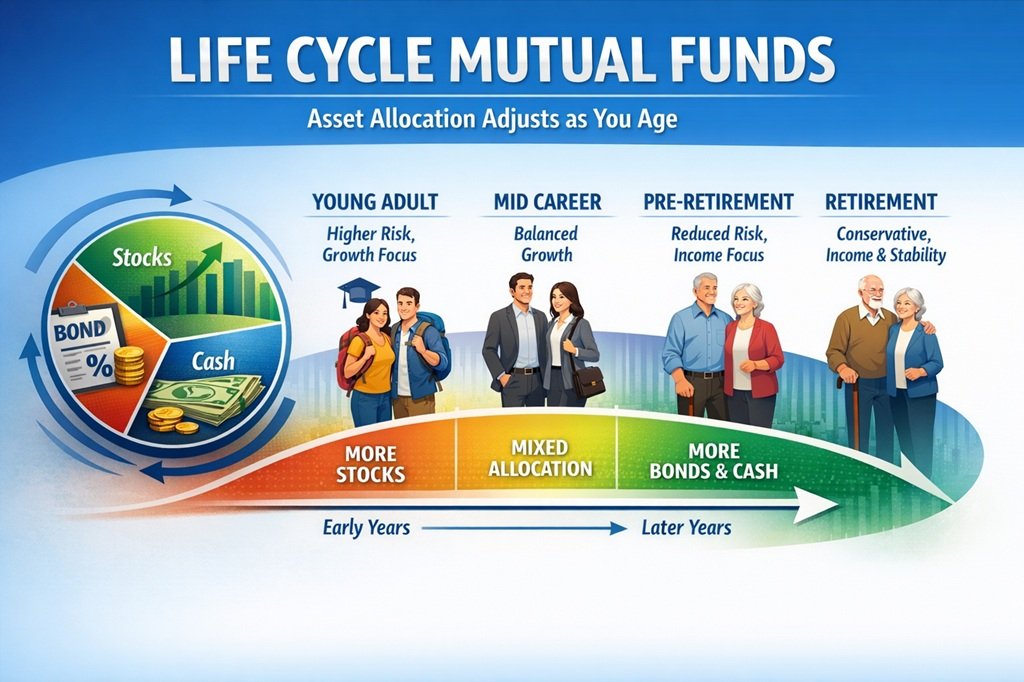

Life Cycle Funds are open-ended mutual funds. That means you can buy or sell units anytime, but they’re built around a set time frame. The idea is simple: You pick a fund based on when you need the money. For example, if you’re planning for something 10 years from now, you choose a 10-year fund. As time passes, the fund automatically changes how it invests your money. It starts with more risk when you’re young or far from your goal, and then shifts to safer options as you get closer. This is called a “glide path” strategy.

Think of it like driving a car. When you’re far from home, you might speed up on the highway (that’s like investing in stocks for higher growth). But as you near your neighborhood, you slow down and take safer roads (like switching to bonds or fixed-income stuff). This helps avoid big losses right when you need the cash.

These funds aren’t just limited to stocks and bonds. They can put money into a mix of things: equity (which means company shares), debt (like loans or bonds), InvITs (that’s Infrastructure Investment Trusts, which are like owning parts of roads or power plants), exchange-traded commodity derivatives (fancy way of saying bets on prices of things like oil or metals), and even gold and silver ETFs. ETFs are exchange-traded funds, which are like baskets of assets you can buy and sell on the stock market. Gold and silver ETFs let you invest in precious metals without actually holding the physical stuff.

By spreading money across these, the funds aim to balance risk and reward. SEBI wants to make goal-based investing straightforward. Goal-based means tying your savings to real-life targets, not just throwing money into the market and hoping for the best. For instance, a young parent might use a 20-year fund for their kid’s college fees. Or someone in their 40s could pick a 15-year one for retirement. It’s all about matching the fund’s timeline to your life’s milestones.

How Long Do These Funds Last? The Tenure Details

One of the key features is the length of time these funds run. SEBI says mutual fund companies can offer Life Cycle Funds with tenures from 5 years up to 30 years. They have to be in steps of 5 years—so options like 5, 10, 15, 20, 25, or 30 years. No weird numbers in between. And each fund house (that’s what we call mutual fund companies) can only have up to six of these funds open for new investors at once. That keeps things from getting too cluttered.

The name of the fund has to include the year it matures. Mature means when the fund ends and you get your money back or it shifts elsewhere. So, if you invest in 2026 for a 20-year fund, it might be called “Life Cycle Fund 2046.” That way, everyone knows exactly when it’s supposed to wrap up.

What happens as the end gets near? If a fund has less than a year left, the company can merge it into the closest other Life Cycle Fund. But they need your okay first—something called “positive consent” from unitholders (that’s you, the investor). This merger helps keep things smooth and avoids small funds that are hard to manage.

I should mention that these are long-term tools. SEBI doesn’t want people jumping in and out quickly. That’s why there’s an exit load, which is like a fee for leaving early. More on that later.

The Glide Path: How Your Money Shifts Over Time

The heart of these funds is the glide path. It’s a plan that decides how much of your money goes into risky stuff versus safe stuff, and it changes automatically as years go by.

In the beginning, when the fund has a long time left (say, 20-30 years), it might put 80-100% into equities. Equities can grow a lot but can also drop sharply, like during a stock market crash. That’s okay when you’re far from needing the money because there’s time to recover.

As time ticks down, the fund slowly moves money out of equities and into debt instruments. Debt is steadier—like government bonds or corporate loans that pay interest regularly. By the last few years, maybe only 20-40% is in equities, and the rest is in safer spots.

There’s a special rule for funds with less than 5 years to go. They can add up to 50% in equity arbitrage. Arbitrage is a low-risk way to make money by buying and selling the same thing in different markets at slightly different prices. This keeps the total equity exposure between 65% and 75%. It’s a way to add a bit more potential growth without too much danger.

These funds follow benchmarks similar to Multi-Asset Allocation Funds. A benchmark is like a yardstick to measure performance against. For example, it might compare to a mix of stock indexes, bond indexes, and commodity prices.

Why does this matter? Many people struggle with rebalancing their portfolios. Rebalancing means adjusting your investments back to the original plan if one part grows too much. It’s easy to forget or get emotional—selling when prices are low out of fear, or buying high out of greed. Life Cycle Funds do this for you, which can lead to better results over time.

Let me give an example. Suppose Raj is 35 and wants to retire at 60. That’s 25 years away. He picks a 25-year Life Cycle Fund. Early on, it’s heavy in stocks from growing companies in India, maybe some international ones too. As he hits 50, the fund starts buying more bonds from stable firms or the government. By 59, it’s mostly safe stuff, protecting his nest egg from market dips.

Exit Loads

To make sure people think long-term, SEBI set up exit loads. These are charges if you pull your money out early.

- If you leave within the first year: 3% fee.

- Within two years: 2%.

- Within three years: 1%.

After three years, no fee. It’s like a gentle nudge: “Hey, stick around for the full ride to get the most benefit.” This discourages short-term trading and helps the fund managers plan better.

Compare this to regular mutual funds, where exit loads might be lower or none. But here, it’s tied to the goal-based idea. If you’re saving for a house in 10 years, why cash out after six months? That could mess up your plans and cost you extra.

Saying Goodbye to Old Solution-Oriented Funds

SEBI isn’t just adding new funds; they’re cleaning house. The old category called solution-oriented funds is gone, effective immediately. This included retirement funds (for your golden years) and children’s funds (for education or marriage).

If you already have money in those, don’t worry. They won’t accept new investments, but existing ones will keep running for now. Fund houses have to merge them into other similar schemes. Similar means matching the risk and asset mix. SEBI has to approve these mergers to ensure fairness.

Why the change? Experts say the old funds didn’t always work well. People sometimes treated them like regular funds, not tying them to goals. Plus, they had lock-in periods (like 5 years for retirement funds), which could be inflexible. Life Cycle Funds fix that with the glide path and flexible tenures.

Market folks are excited. One industry leader said it’s a big step for retail investors—those everyday people like you and me, not big institutions. It tackles “behavioral challenges,” meaning our bad habits like panicking during market falls. By automating things, it promotes discipline.

Broader Benefits

Let’s talk about why this is good news. First, it’s tax-efficient. In India, long-term capital gains on equities (held over a year) are taxed at 12.5% above Rs 1.25 lakh. Debt has different rules. The glide path might help optimize taxes as the fund shifts.

Second, it’s great for beginners. You don’t need to be a finance whiz. Just pick your timeline, invest regularly (maybe through SIPs—systematic investment plans, where you put in a fixed amount monthly), and let it roll.

Third, including things like gold ETFs adds diversification. Gold often goes up when stocks go down, acting like a safety net. InvITs give exposure to infrastructure, which is booming in India with all the roads and airports being built.

But nothing’s perfect. Risks? Markets can be volatile. If equities crash early on, your fund might take a hit. Also, fund managers aren’t always right—though SEBI regulates them tightly. Fees matter too; these funds might have expense ratios (annual charges) around 1-2%, eating into returns.

Inflation is another factor. If prices rise fast, your money needs to grow enough to keep up. A 30-year fund assumes you’ll need it then, but life changes—job loss, health issues. So, review your investments yearly.

How does this compare globally? In the US, they have target-date funds, similar idea, popular in 401(k) plans. India’s version is tailored to our market, with local assets.

Industry reactions? Positive overall. One executive called it a “structural reform.” It could boost mutual fund inflows, already growing fast in India. As of 2026, the industry manages trillions in assets, with more people joining via apps.

Is a Life Cycle Fund Right for You?

SEBI’s Life Cycle Funds are a fresh take on saving smartly. They’re for anyone with a clear goal and timeline—retirement, home buying, travel dreams. By automating the tough parts, they reduce stress and mistakes.

If you’re interested, talk to a financial advisor. Check fund prospectuses for details on exact allocations and past performance (though new, similar funds exist). Start small, maybe with a 5-year one for a short goal like a vacation.

In the end, investing is about patience and planning. These funds make that easier. As India’s economy grows, tools like this help more people build wealth safely. Keep an eye on updates from SEBI—they’re always tweaking for better investor protection.

{kind=link}