Investing your hard-earned money is one of the most important financial decisions you will ever make. Most people in India today want their money to grow faster than what a simple savings account or fixed deposit can offer. Two of the most talked-about options are Smallcase and Mutual Funds. At first glance, both seem to do the same job — they let you put money into a collection of stocks or other assets without having to pick and manage every single stock yourself. But once you dig a little deeper, you realise they work in completely different ways, suit different kinds of people, and come with their own advantages and disadvantages.

In this detailed guide, we will walk through everything you need to know in the simplest possible language. By the end, you will be able to decide clearly which one fits your goals, your risk comfort, and how much time you actually want to spend watching the market.

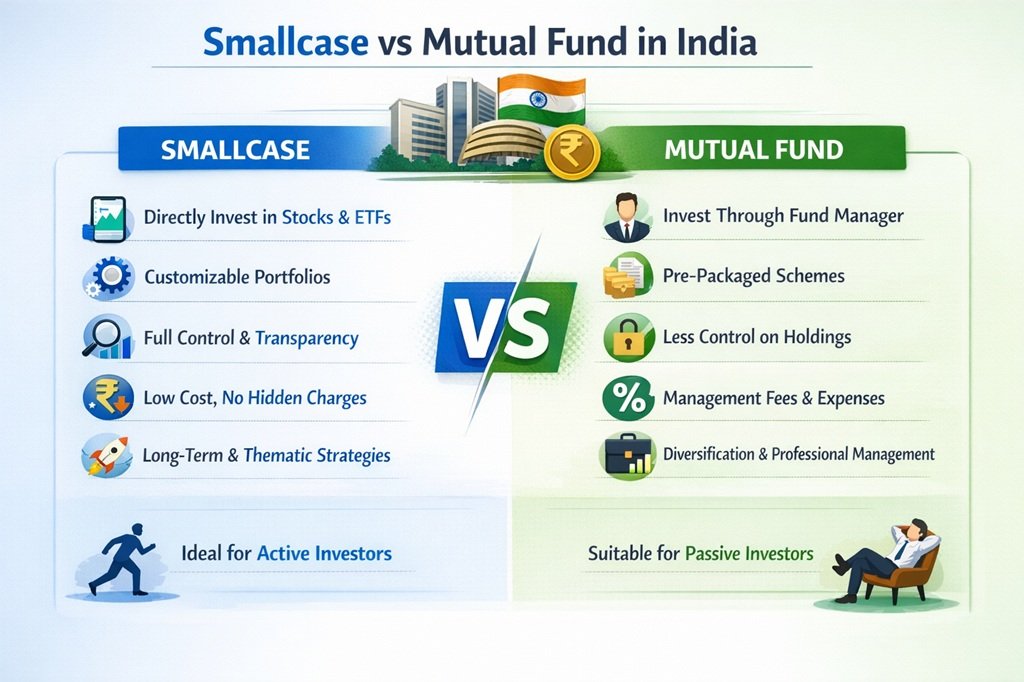

What Exactly Is a Smallcase?

A smallcase is like a ready-made basket of stocks or exchange-traded funds (ETFs). Each basket follows one clear idea, theme, or strategy. For example, there might be a “Dividend Kings” smallcase with companies that pay steady dividends every year. Or a “Green Energy” smallcase with companies building solar panels and electric vehicles.

The idea started around 2015 when a company called smallcase (the platform) made it easy for regular people to invest this way. Today in 2026, there are more than 500 different smallcases created by SEBI-registered experts. You don’t buy one stock. You buy the whole basket in one click, and every stock in that basket goes straight into your own demat account.

Think of it like buying a pre-packed gift hamper instead of picking each item from different shops. The hamper (smallcase) is already put together by someone who knows what goes well together.

Here is how it actually works in real life:

- You open a demat and trading account (with Zerodha, Groww, Upstox, Angel One, etc.).

- You go to the smallcase platform or your broker’s app.

- You pick a smallcase you like.

- You invest a minimum amount (usually ₹5,000 or ₹10,000).

- The stocks are bought and appear in your demat account within minutes.

- You own those shares directly. You can see the price moving live. You can sell one company if you want, or add more.

This direct ownership is the biggest difference from mutual funds.

Key Features of Smallcase That Make It Special

- Full transparency — You always know exactly which 10–50 stocks you own and how much of each.

- You can customise — Many people remove one stock they don’t like or add their favourite company.

- Rebalancing — The manager updates the basket once or twice a year. You can accept the changes or skip them.

- Thematic investing — You can pick themes like “Rural India growth”, “Tech revolution”, “Healthcare boom”, “ESG” (environment, social, governance), or even “Zero Debt Companies”.

- Low or no annual fees in many cases — Some smallcases are completely free. Others charge a one-time fee or small yearly subscription (₹100–500 per year).

- You can start small — Many good smallcases need only ₹10,000 to begin.

Real Advantages of Investing in Smallcase

People who love smallcases usually say things like:

“I feel like I actually own the companies, not just some units in a fund.”

“Because I can see every stock, I understand my money better.”

“In bull markets, thematic smallcases can give much higher returns than broad mutual funds.”

“You can exit only the stocks you don’t want anymore. No need to sell everything.”

“Costs are often lower because there is no big expense ratio eating your returns every year.”

Many young investors in their 20s and 30s prefer smallcases because they like learning about the market and want control.

The Honest Downsides of Smallcase

But it is not perfect. Here are the real problems:

- Higher risk — Most smallcases are concentrated in one theme. If that theme does badly (for example, IT stocks in 2022), your money can fall 30–40% in a few months.

- You need to keep an eye — You should check your portfolio every few months. If the manager rebalances, you have to decide whether to follow.

- Taxes can hurt more — Every time you rebalance or sell a stock, you pay capital gains tax. Frequent changes mean more tax bills.

- Not for complete beginners — If you panic when the market falls, this can be stressful.

- Brokerage charges — You pay brokerage every time the basket is bought or rebalanced.

What Are Mutual Funds?

Mutual funds are like a big shared pot. Thousands of people put money into the same pot. A professional fund manager uses that money to buy hundreds of stocks, bonds, or a mix of both. You don’t own the individual stocks. You own “units” of the fund. The value of your units is called Net Asset Value (NAV) and it is calculated every day.

Mutual funds have been around in India since 1963, but they really took off after 2009 when SIPs became popular. Today there are more than 2,000 mutual fund schemes.

Types you will hear about:

- Equity funds — Mostly stocks, higher risk and higher returns.

- Debt funds — Mostly bonds and fixed-income, safer.

- Hybrid funds — Mix of stocks and bonds.

- Index funds — Copy the Nifty 50 or Sensex exactly (very low cost).

- Thematic/sector funds — Similar to smallcases but managed by the fund house.

How it works:

You invest through SIP (₹500 per month) or lump sum. The fund manager buys and sells stocks for you. You never see the individual shares. At the end of the day, you get the NAV price whether you buy or sell.

Why Millions of Indians Love Mutual Funds

- Super simple — Set a SIP and forget. No need to check every day.

- Excellent diversification — One fund can have 50–100 stocks across sectors.

- Professional management — Experienced managers with teams of analysts work full-time.

- Low minimum — Start with ₹500 per month.

- SIP advantage — Rupee-cost averaging. You buy more when prices are low.

- Regulated and safe — SEBI watches them strictly. Money is safe even if the fund house has problems.

The Real Problems with Mutual Funds

- No control — You cannot remove a stock you dislike (like a company in controversy).

- Expense ratio — Every year 0.5% to 2.5% is deducted. Over 20 years this can reduce your final amount by lakhs.

- Limited transparency — You get the list of holdings only once every month, and it is always a few days old.

- Exit can be slow — You sell at end-of-day NAV. In bad markets, you cannot sell at the price you see right now.

- In bull markets, active funds sometimes lag behind pure thematic plays.

Smallcase vs Mutual Funds: Side-by-Side Comparison (2026 Updated)

Here is a clear table with extra explanations below.

| Basis | Smallcase | Mutual Funds |

| Ownership | Direct stocks in your demat account | Units of the fund |

| Control | High — you can customise, add, remove | Very low — manager decides everything |

| Transparency | 100% — you see every stock live | Limited — monthly disclosure |

| Minimum investment | Usually ₹5,000–₹25,000 | As low as ₹500 via SIP |

| Cost | Brokerage + small subscription (often low) | Expense ratio 0.5–2.5% every year |

| Risk | Higher (thematic, concentrated) | Varies — debt funds low, equity high |

| Liquidity | Sell any time during market hours | Redeem at end-of-day NAV |

| Taxation | Like stocks — LTCG 12.5% after 1 year | Equity funds same as smallcase |

| Best for | Active, informed investors | Beginners, passive, long-term investors |

Let me explain the most important rows a bit more.

Cost — Suppose you invest ₹1 lakh. A mutual fund with 2% expense ratio takes ₹2,000 every year. A smallcase might cost you ₹200–500 brokerage once a year. Over 10 years the difference is huge.

Liquidity — If the market crashes and you want to sell immediately, in smallcase you can sell the stocks you want right away. In mutual funds you have to wait till evening.

Tax — Both are equity investments, so rules are similar now (after 2024 budget changes). But smallcase rebalancing creates more taxable events.

Performance — Which One Gives Better Returns?

This is the question everyone asks. The answer changes every year.

In strong bull markets (like 2020–2021 or 2023–2024), thematic smallcases often beat broad mutual funds by 5–15% because they catch the hot sectors early.

In sideways or bear markets, diversified mutual funds lose less money.

Average long-term (10+ years) returns for good equity mutual funds are around 12–15%. Good smallcases have shown 15–25% in some periods, but with bigger drops.

Past performance never guarantees future results. Always remember that.

Who Should Choose Smallcase?

- You are below 40 and can handle 30–40% drops without selling.

- You like reading about companies and want to learn.

- You have at least ₹50,000–1 lakh to invest at once.

- You want to follow specific themes like EV, AI, defence, or consumption boom.

Who Should Choose Mutual Funds?

- You are new to investing.

- You want to invest small amounts every month via SIP.

- You hate seeing red numbers and want peace of mind.

- You are saving for goals like child’s education or retirement and don’t want to touch the money for 10+ years.

Can You Invest in Both?

Yes! This is what many smart investors do in 2026.

Put 60–70% in broad mutual funds or index funds for safety and steady growth. Put 30–40% in 2–3 good smallcases for higher potential returns and fun.

This way you get the best of both worlds — stability + excitement.

How to Start Today

- Open a demat account if you don’t have one (takes 1 day online).

- For mutual funds — use Groww, Zerodha Coin

- For smallcase — go to smallcase.com or your broker app.

- Start with ₹5,000–10,000 in one or two options.

- Review once every 6 months.

Final Thoughts

There is no single “best” option. Smallcase is like driving your own car — you control the steering but you also feel every bump. Mutual funds are like hiring a professional driver — comfortable ride, but you don’t choose the route.

In 2026, with technology making everything easier, both are excellent choices. The real winner is the person who starts investing early, stays disciplined, and chooses what matches their personality.

If you are still confused, start small with both. Put ₹2,000 in a Nifty index fund SIP and ₹3,000 in one smallcase. After 6 months you will know what feels right for you.

Frequently Asked Questions

Is smallcase better than mutual funds?

Not always. It depends on your risk appetite and involvement level.

Are mutual funds safer?

Generally yes, because of wider diversification and professional management.

Can beginners start with smallcase?

Yes, but it is better to start with index funds first and learn slowly.

Which has better returns?

Smallcase can give higher returns in good market conditions, but mutual funds are more consistent.

Can I withdraw anytime?

Smallcase — yes, during market hours. Mutual funds — yes, but at end-of-day price.

Tax on smallcase vs mutual fund?

Almost the same for equity investments now.

Remember, investing is a marathon, not a sprint. The most important thing is to start and keep learning. Your future self will thank you.

(Disclaimer: This is for educational purposes only. Investing involves risk of loss. Please consult a financial advisor before investing.)

If you found this helpful, share it with a friend who is also thinking about investing. Happy investing!

{kind=link}