Picture this: You’re in a rush, tapping away on your phone to send money to a friend for splitting that weekend dinner bill. You hit confirm, and bam—only then do you notice the UPI ID was off by one digit. Your heart sinks as the money zips off to some stranger’s account. Sound familiar? In India’s buzzing digital payment world, where UPI handles billions of transactions every month, these little slip-ups happen more often than you’d think. But here’s the good news: it’s often possible to reverse wrong UPI transactions if you act fast and follow the right steps.

We’ve all been there, rushing through payments without double-checking. Yet, understanding how to reverse wrong UPI transactions can turn a potential headache into a manageable fix. This guide breaks it all down in simple terms—no jargon overload, just straightforward advice. We’ll cover everything from spotting the mistake early to escalating if needed, drawing from real processes used by banks and apps today. By the end, you’ll feel more confident navigating these bumps in the road. Let’s dive in!

Why Do Wrong UPI Transactions Happen Anyway?

Mistakes with UPI aren’t usually some big conspiracy; they’re just human errors amplified by how fast everything moves these days. You’re juggling a call, kids, or traffic, and suddenly that payment’s gone to the wrong place. Common culprits include typing a wrong phone number or UPI ID—maybe you swapped a 7 for a 1 without noticing. Or perhaps you scanned a QR code that looked right but wasn’t.

Then there are those sneaky similar names. Ever noticed how many people have VPAs like “rahul@upi” or “rahul123@upi”? If you’re sending to “Rahul Kumar” but pick the wrong one from your history, oops! Technical glitches play a role too, though they’re rarer—network hiccups or app lags might cause a mix-up.

And let’s not forget fraud, where scammers trick you into sending money via fake links or urgent pleas. But even honest errors can sting. The key takeaway? These things occur because UPI is designed for speed, not foolproof perfection. That’s why knowing how to reverse wrong UPI transactions is a lifesaver.

Spotting and Reacting to a Wrong Transfer

Catching the error early is half the battle won. The moment that “successful” notification pops up, pause and verify. Check the recipient’s name that flashes on screen—most apps like Google Pay or PhonePe show it before you enter your PIN, and again after.

If something feels off, don’t wait. Screenshot everything: the transaction ID, amount, date, and recipient details. This proof will be gold when you’re trying to reverse wrong UPI transactions later.

Now, breathe. Panicking won’t help, but quick action will. Start by trying the simplest fix—reaching out to the recipient if possible. Sometimes the UPI ID links to a phone number, or you might recognize the name. A polite message like, “Hey, I think I sent money to you by mistake—could you please send it back?” works wonders if they’re honest. Surprisingly often, people do return it voluntarily!

But if that’s not an option, move to formal channels right away. Delaying even a day reduces your chances, especially if the receiver withdraws the cash.

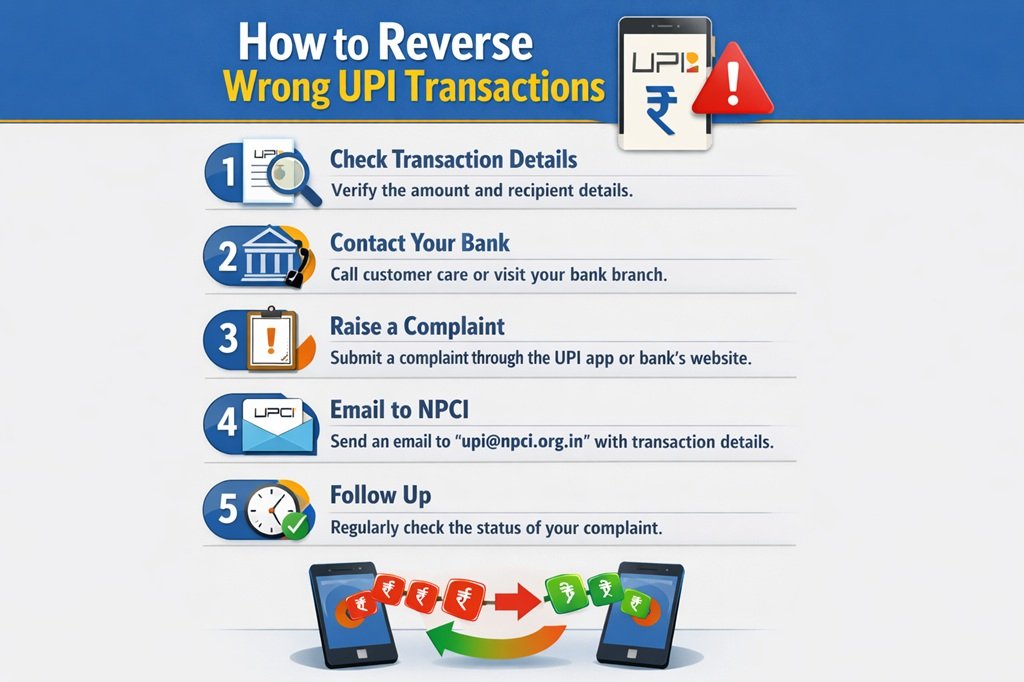

How to Reverse Wrong UPI Transactions Through Your App

Most of us use apps like Google Pay, PhonePe, Paytm, or BHIM for UPI. Luckily, they all have built-in ways to report issues. Here’s how to kick off the process to reverse wrong UPI transactions:

- Open your app and head to transaction history.

- Find the dodgy payment and tap on it.

- Look for options like “Report an Issue,” “Raise Dispute,” “Help & Support,” or “Need More Help.”

- Select the reason—usually something like “Sent to wrong person” or “Incorrect beneficiary.”

- Fill in details: explain what happened, add any screenshots, and submit.

For specifics:

Google Pay:

- Tap the transaction > “Contact” or “Report a problem” > Choose “Payment went to wrong person.”

PhonePe:

- Go to history > Select transaction > “Report Issue” > Pick the category and describe.

Paytm:

- Transaction details > “Help” > “Report a Payment Issue.”

BHIM:

- Similar flow—select and raise concern.

The app forwards your complaint to your bank, who then contacts the receiver’s bank. If the funds are still there and it’s a clear mistake, reversal can happen in days. Acting within 24-48 hours boosts success big time.

Getting Your Bank Involved in Reversing Wrong UPI Transactions

If the app route drags on or doesn’t resolve things, loop in your bank directly. After all, they’re the ones holding the strings.

Call customer care (have your transaction ID ready) or visit a branch. Explain calmly: “I made a wrong UPI transfer—here are the details.” They’ll register a formal complaint and might place a lien on the receiver’s account to freeze the money temporarily.

Banks follow NPCI guidelines, so they can’t force a reversal without cooperation, but they can pressure the other side. In genuine errors, many receivers agree to return it once contacted. Your bank coordinates with the recipient’s bank, and if everything checks out, you’ll see the money back in your account soon.

Pro tip: Keep a reference number from every call or visit. It helps track progress when learning how to reverse wrong UPI transactions.

When You Need Bigger Help to Reverse Wrong UPI Transactions

Things still stuck after dealing with your app and bank? Time to bring in the big guns—NPCI, the folks running UPI.

Head to their website and find the Dispute Redressal section. Or call the helpline at 1800-120-1740. Provide all details: transaction ID, banks involved, what you’ve done so far.

NPCI investigates, liaising between banks. Recent updates have made chargebacks faster, especially for clear-cut errors. Resolutions can take 7-15 days, but it’s structured and fair.

This step is crucial for stubborn cases. Many people successfully reverse wrong UPI transactions here after lower levels fail.

What If It’s Fraud? Extra Steps for Suspicious Wrong Transfers

Not all wrong transfers are accidents. If it smells like a scam—fake urgent requests, unknown links—treat it differently.

Report to cybercrime.gov.in immediately, filing a complaint with transaction proof. This freezes trails faster.

Still follow the app/bank/NPCI path, but mention fraud. Banks might reverse quicker if funds haven’t moved.

And if it’s a big amount with no resolution, escalate to the RBI Ombudsman—free and effective mediation.

How Long to Reverse Wrong UPI Transactions?

Patience is key, but so is knowing expectations.

- Same bank: Often 24-48 hours.

- Different banks: 5-10 working days typically.

- With NPCI: Up to 15-30 days.

No strict deadline to report, but sooner is better—ideally within days. Funds withdrawn? Recovery gets tougher, as reversal needs receiver consent or proof of error/fraud.

Success isn’t guaranteed, especially if the receiver refuses. But most honest mistakes get fixed.

Tips to Avoid Needing to Reverse Wrong UPI Transactions

We’ve focused on fixes, but let’s talk avoidance. It’s way less stressful!

- Always verify the name that pops up before PIN.

- Use “Check Balance” or small test transfers for new IDs.

- Save frequent contacts properly.

- Avoid rushing—take that extra second.

- Enable notifications and review history regularly.

Simple habits go a long way in dodging these mishaps.

How People Successfully (or Not) Reversed Wrong Transfers

Hearing from others makes it relatable. Take Raj from Mumbai—he sent ₹5,000 to a wrong “priya@upi” instead of his sister’s. Panicked, he contacted the receiver via linked phone (luckily visible). She returned it same day!

Or Sarah, who typo’d a vendor’s ID. App dispute didn’t work fast, so she went to her bank. After NPCI escalation, money back in two weeks.

On the flip side, delays cost some folks when receivers spent the cash quickly. Lesson? Speed matters.

FAQs

Can a successful UPI transaction be reversed automatically?

No, not usually. Once PIN-entered, it’s final. But disputes can lead to manual reversal.

What’s the best time to report a wrong UPI transfer?

As soon as you notice—ideally within hours. 24-48 hours greatly improves odds.

Do I need to go to police for every wrong transfer?

Only if it’s fraud or large amount with no cooperation. For honest mistakes, app/bank/NPCI first.

Will I get charged for raising a dispute to reverse wrong UPI transactions?

Typically no—it’s free through apps, banks, and NPCI.

What if the receiver ignores requests?

Banks can lien the amount during investigation. NPCI or Ombudsman can push further.

Is it easier to reverse wrong UPI transactions in 2025?

Yes! Recent NPCI updates have streamlined chargebacks, making resolutions quicker for genuine cases.

Can I trace the wrong recipient’s details?

Limited—apps show name, sometimes phone. Banks/NPCI handle deeper traces during disputes.

What documents do I need?

Transaction ID, screenshots, bank statements. Keep them handy!

Conclusion

Wrapping up, messing up a UPI payment feels awful in the moment, but it’s rarely the end of the world. With clear steps—from checking details upfront to contacting apps, banks, and NPCI—you’ve got solid tools to reverse wrong UPI transactions. The system’s designed to protect users, especially when you act swiftly and stay calm.

Remember, millions zip money daily without issues because they pause to verify. Adopt that habit, and you’ll rarely need this guide. But if you do? You’ve got this. Stay safe out there in the digital payment jungle—happy (and accurate) transacting!

{kind=link}