We invest our money in various asset classes to earn returns. But most of us don’t know correct way to calculate returns. For example

- Mr. Anil invested Rs 20,000 in a mutual fund and 2 years of holding it became Rs 40,000

- Mr. Sunil invested Rs 50,000 in Gold for 6 years and it became Rs 4,00,000

Who has earned better returns? & what method we should use to calculate returns so that we do not end up comparing apple to oranges! We are herewith article showing correct ways to compare returns with formulas and examples.

Also Read – Home Loan EMI Calculator Prepayment and Closure

What is Return on Investment?

Return is the gain or loss in the value of an asset in a particular period. It is usually mentioned as a percentage. The general rule is that the more risk you take, the greater the potential for higher return and loss. Return on investment has two basic components.

- Interest and/or dividends, the income generated by the underlying investment.

- Appreciation (Depreciation), an increase (decrease) in the value of the investment.

Why finding return on investment is important:-

- Determining return on investment is an important part of investment review to know whether your investments are on track and make appropriate adjustments.

- Estimating a return on investment also helps in choosing among investment options – One should invest in Gold/Real Estate/Stocks/Mutual Funds/Fixed Deposits ?

Let’s learn about various kinds of returns!

Absolute return (Point to Point Returns): Absolute return is the increase or decrease that an investment achieves over a given period of time expressed in percentage terms. It’s calculated as follows:

Absolute returns = 100* (Selling Price – Cost Price)/ (Cost Price)

For example you invested in asset in February 2006 at a price of Rs 20000. And you sold the investment in November 2012 at the cost of Rs 42000. Absolute returns in this case will be:

Absolute returns = 100* (42000 – 20000)/20000 = 110%

This is most simple method to calculate returns but it does not consider time period. That is where real catch is. Most of time this method produces a large number so people are impressed!

Simple Annualized Return: The increase in value of an investment, expressed as a percentage per year. Expressed as –

Simple Annualized Return= Absolute Returns/Time period.

Suppose investment of Rs 1,00,000 becomes 1,24,000 over three years.

Absolute return = 100* ( 124000 – 100000/100000 ) =24 %.

Simple annualized return = 24/3 = 8 %

Average Annual Return (AAR)

Average annual return (AAR) is the arithmetic mean of a series of rates of return. The formula for AAR is:

AAR = (Return in Period 1 + Return in Period 2 + Return in Period 3 + …Return in Period N) / Number of Periods or N

Also Read – Capital Gain Tax Calculator – Download

Let’s look at an example. Assume that an investment XYZ records the following annual returns:

| Year | Annual Return |

| 2005 | 20% |

| 2006 | 25% |

| 2007 | 22% |

| 2008 | -10% |

AAR for the period from 2005 to 2008: = (20% + 25% + 22% -10%) / 4 = 57%/4 = 14.25%

AAR is somewhat useful for determining trends. AAR is typically not regarded as a correct form of return measurement and thus it is not a common formula for analysis.

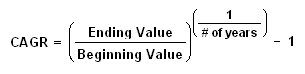

Compound Annual Growth Rate or CAGR

CAGR is the year-over-year growth rate of an investment over a specified period of time. It’s an imaginary number that describes the rate at which an investment would have grown if it grew at a steady rate.

Let’s assume you invested Rs 10,000 in Apr 2010 and by Apr 2011 your investment became Rs 30,000, by Apr 2012 it became Rs 15,000. What was the return on your investment for the period?

If you calculate absolute return than it is 50% & simple annualized return is 25%.

But this investment return has fluctuated over a period of time, so how to make estimation that if you have continued investing in same asset class it would have given better result or not. This is similar to saying that you went on a trip and averaged 60 km/hr. Whole time you did not actually travel 60 km/hr sometimes you were traveling slower, other times faster.

So CAGR is a way to smoothen out the returns, it determines an annual growth rate on an investment whose value has fluctuated from one period to the next. In that sense CAGR isn’t the actual return in reality.

Also Read – PPF Account Calculator Download

The formula to calculate CAGR is:

CAGR Formula

So CAGR for above example is :

= ((15,000/10,000) ^ (1/2)) -1

= 22.47%

If the investment states that it had an 8% annualized return over ten years, that means if you invested on Apr 1, and sold your investment on Mar 31 exactly ten years later, you earned the equivalent of 8% a year. However, during those ten years, one year the investment may have gone up 20% and another year it may have gone down 10%. In the example if the investment Rs 10,000 would have grown at the rate of 22.47% every year and at end of two years it would be Rs 15,000 as shown in calculation below.

| Year | Initial Value | Growth | Final Value |

| 1 | 10,000 | 2,247 | 12,247 |

| 2 | 12,247 | 2752 | 15,000 |

Good and Bad of CAGR: CAGR is the best formula for evaluating how different investments have performed over time. Investors can compare the CAGR in order to evaluate how well one stock/mutual fund has performed against other stocks in a peer group or against a market index. The CAGR can also be used to compare the historical returns of stocks to bonds or a savings account. But the bad points of CAGR are:

- CAGR does not reflect investment risk, and you must use the same time periods.

- CAGR does not reflect volatility. Investment returns are volatile, they can vary significantly from one year to another. CAGR give the illusion that there is a steady growth rate even when the value of the underlying investment can vary significantly.

Please remember that returns that we have looked at so far are using value of investment at beginning and at end of the period. But it does not tell the full story. So what is to be done in order to know full story.

Check out next article Calculating Returns of Investment – Formulas & Examples – 2 to know full story explaining Rolling Returns, Relative Returns, IRR and XIRR.

{kind=link}