UPI, which stands for Unified Payments Interface, is an instant digital payment platform enabling users to transfer funds, settle bills, and handle accounts using a single application.

Have you ever made a payment just by scanning a QR code? Or transfer money instantly without entering lengthy bank details? If yes, you’ve already experienced the power of UPI! Unified Payments Interface (UPI) has revolutionized the way we handle transactions, making payments seamless, instant, and secure. But what exactly is UPI, and how does it work? Let’s dive in!

What is UPI?

UPI, or Unified Payments Interface, is a real-time payment system developed by the National Payments Corporation of India (NPCI). It enables users to transfer funds instantly between bank accounts via mobile phones. Think of it as a digital wallet, but even better—it directly links to your bank account, eliminating the need to preload money.

UPI removes the requirement to input extensive bank details for every transaction, streamlining payments via QR codes, virtual payment addresses (VPAs), or mobile numbers registered with UPI.

UPI functions by utilizing current systems like the Immediate Payment Service (IMPS) and the Aadhaar Enabled Payment System (AEPS) to facilitate smooth payment settlements between bank accounts.

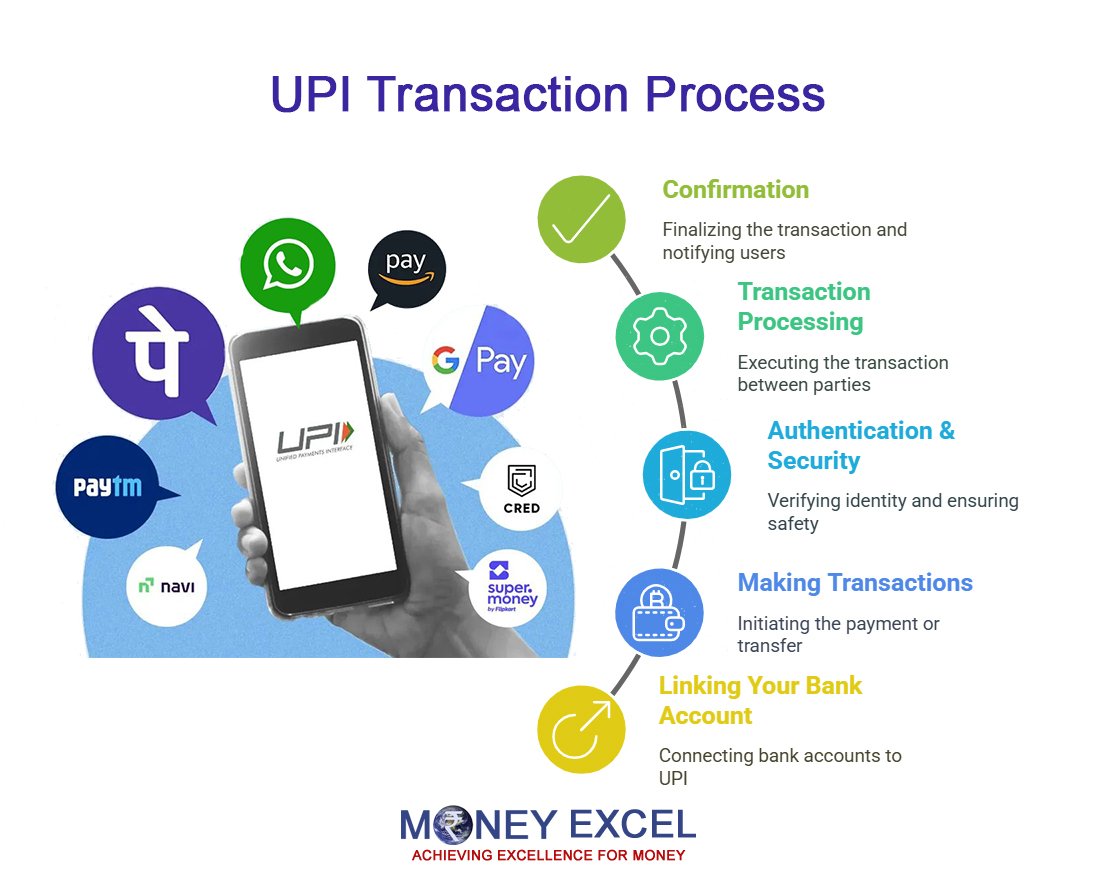

How Does UPI Work?

1. Linking Your Bank Account

UPI works by linking your bank account to a unique Virtual Payment Address (VPA), also called a UPI ID. This eliminates the need to share bank details every time you make a transaction. Following installation, users register by connecting their bank account and setting up a distinct virtual payment address (VPA), for example, user@bankname, which functions as their UPI ID.

2. Making Transactions

When a user intends to complete a payment, they have the option to choose the payee’s VPA (e.g., merchant@bankname), scan a QR code, or input their UPI ID. For example, if a consumer intends to pay a local vendor, they can easily scan the vendor’s QR code or input the vendor’s VPA.

UPI enables multiple types of transactions:

- Peer-to-Peer (P2P) Transfers – Sending money to friends and family.

- Merchant Payments – Paying for goods and services online and offline.

- Bill Payments – Utility bills, subscriptions, and more.

- Fund Requests – Requesting payments from others.

3. Authentication & Security

Every UPI transaction is secured by a two-factor authentication system:

- UPI PIN: A 4-6 digit code set by the user.

- Mobile Number Verification: Transactions work only from registered mobile numbers.

To authorize the transaction, users need to input their UPI PIN—a secure six-digit code established during the registration process. This process guarantees that solely the account owner can authorize transactions.

4. Transaction Processing

After the UPI PIN is submitted, the application forwards the payment request to the UPI server. The server checks the request and handles it by contacting the user’s bank (the issuer) and the recipient’s bank (the acquirer).

5. Confirmation

Once the banks verify the transaction, the user gets an immediate alert about whether the payment succeeded or failed. The UPI system guarantees that funds are transferred between banks quickly, typically within a few hours, while users notice the transaction in their accounts right away.

This smooth process, enabled by applications like PhonePe, Google Pay, and Paytm, renders UPI an effective, safe, and user-friendly option for digital transactions, helping to its extensive use in India.

Key Features of UPI

1. Instant Transfers

UPI transactions are processed in real-time, unlike traditional NEFT transactions that take a few hours.

2. 24/7 Availability

Forget about bank holidays! UPI operates 24/7, even on weekends and public holidays.

3. No Need for Bank Details

Instead of sharing your account number and IFSC code, you only need a UPI ID or mobile number linked to the recipient’s account.

4. QR Code Payments

UPI supports QR code-based payments, making it easy to pay at local stores, restaurants, and street vendors.

5. Multi-Bank Support

You can link multiple bank accounts to a single UPI app and choose which account to use for transactions.

6. Recurring Payments

With the UPI AutoPay feature, users can set up automatic payments for subscriptions, EMIs, and more.

7. Split Bills with Friends

UPI allows users to split expenses with friends and send requests for shared payments.

8. High Transaction Limits

UPI supports large transactions, typically capped at Rs. 1-2 lakh per transaction, depending on the bank.

Popular UPI Apps in India

1. Google Pay (GPay)

Google Pay is one of the most widely used UPI apps, offering seamless transactions and cashback rewards.

2. PhonePe

Owned by Flipkart, PhonePe provides UPI payments, bill payments, and even investment options.

3. Paytm

Initially a digital wallet, Paytm now integrates UPI for instant payments.

4. BHIM UPI

The official UPI app by NPCI, offering a simple interface for direct bank transactions.

5. Amazon Pay

Amazon Pay uses UPI for payments on its e-commerce platform and bill payments.

Major UPI Apps

| UPI App/PSPs | Sponsor Banks | Handles |

| Google Pay | Axis | @okaxis |

| ICICI | @okicici | |

| HDFC | @okhdfcbank | |

| SBI | @oksbi | |

| Phonepe | Yes | @ybl |

| ICICI | @ibl | |

| Axis | @axl | |

| Amazon Pay | Axis | @apl |

| WhatsApp Payments | ICICI Bank | @okicici |

| Airtel Payments Bank | Kotak Mahindra Bank | @Kotak |

| Paytm | ICICI Bank | @okicici |

| BHIM (Bharat Interface for Money) | National Payments Corporation of India (NPCI) | @upi |

How to Set Up UPI on Your Phone

Step 1: Download a UPI App

Choose any UPI-enabled app like Google Pay, PhonePe, or BHIM and install it on your smartphone.

Step 2: Register with Your Mobile Number

Ensure the number registered with your bank is the same as the one used for UPI registration.

Step 3: Link Your Bank Account

The app will fetch your linked bank accounts automatically. Choose the primary account for UPI transactions.

Step 4: Set a UPI PIN

You will be prompted to set a UPI PIN, which acts as a security measure for transactions.

Step 5: Start Transacting!

That’s it! Now you can send and receive money instantly using UPI.

UPI vs Other Payment Methods

| Feature | UPI | Credit/Debit Cards | Net Banking | Wallets |

| Instant Transactions | ✅ | ❌ | ❌ | ✅ |

| Requires Bank Details | ❌ | ✅ | ✅ | ❌ |

| Transaction Fees | None | May Apply | May Apply | May Apply |

| Works 24/7 | ✅ | ✅ | ❌ | ✅ |

Security Measures in UPI

1. UPI PIN Protection

Each transaction requires a UPI PIN, making unauthorized access difficult.

2. Fraud Detection & Alerts

Banks and UPI apps monitor unusual activity and send alerts for suspicious transactions.

3. Secure QR Codes

QR codes ensure payment goes to the correct recipient without manual entry.

4. Device Binding

UPI works only on the registered device with the linked mobile number, reducing fraud risks.

Future of UPI

The future of UPI looks incredibly promising. Some upcoming advancements include:

- Cross-Border UPI Transactions: Making international payments possible.

- Voice-Based UPI Payments: AI-driven voice commands for seamless transactions.

- Offline UPI Payments: Transactions without the need for an internet connection.

Conclusion

UPI has completely transformed digital payments in India. Its ease of use, security, and instant transactions make it the preferred payment method for millions. Whether you’re paying bills, shopping online, or splitting dinner expenses, UPI makes it all effortless. If you haven’t already, set up UPI today and experience a new world of digital transactions!

Frequently Asked Questions (FAQs)

1. Is UPI safe to use?

Yes! UPI is highly secure due to two-factor authentication, encrypted transactions, and device binding.

2. Can I use UPI without the internet?

Currently, UPI requires an internet connection, but offline features are being developed.

3. What is the UPI transaction limit?

The limit varies by bank but generally ranges between Rs. 1-2 lakh per transaction.

4. Can I link multiple bank accounts to UPI?

Yes, you can link multiple accounts and select which one to use for each transaction.

5. What happens if I enter the wrong UPI PIN?

If you enter the wrong UPI PIN multiple times, your account may be temporarily blocked for security reasons.

6. How can I reset my UPI PIN?

You can reset your UPI PIN through your UPI app using your debit card details.

7. Are there any charges for using UPI?

Most UPI transactions are free, but some banks may charge for specific services.

8. Can I use UPI on feature phones?

Yes, through USSD-based *99# service, users without smartphones can still use UPI.

9. What happens if my UPI transaction fails?

Failed transactions are usually reversed automatically. If not, you can contact your bank.

10. Can I use UPI for international payments?

Currently, UPI is domestic, but efforts are being made to enable cross-border transactions.

{kind=link}