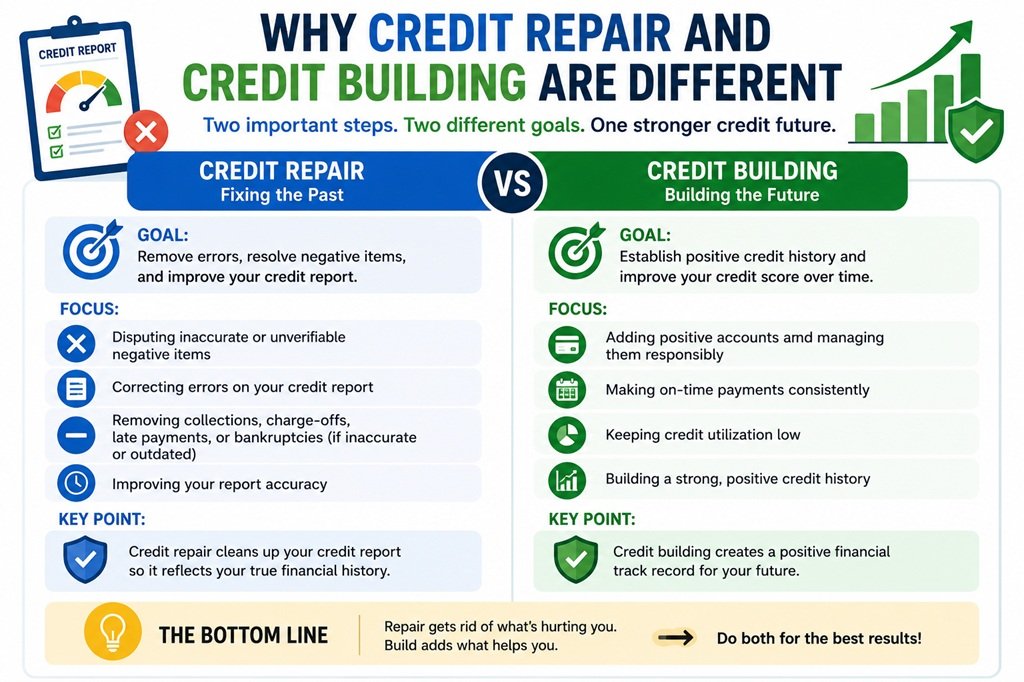

Credit is often treated like a monolith, but there are different strategies for different goals. Improving your score and fixing your credit are not the same thing, and each involves unique steps to success and offers its own challenges.

Credit repair addresses the actual information in your credit file, using your rights to remove mistakes and mitigate negative items. Credit building involves using new credit to create a stronger history. Credit repair and credit building both improve trust with lenders and increase chances of approval, and virtually every consumer will engage in both at some point.

Not focusing on your credit goals can lead to confusion and frustration. A person may spend months trying to build credit when a reporting error is the real problem. Another may focus on disputing negative items while neglecting the habits necessary to build long-term credit strength. Understanding where credit repair ends, and credit building begins can help consumers make better decisions and set more realistic expectations.

What Is Credit Repair?

Credit repair focuses on correcting problems that already exist within a consumer’s credit profile.

Most commonly, this involves reviewing credit reports for inaccurate, incomplete, outdated, or unverifiable information and addressing those issues through the dispute process. The goal is not to create positive credit history. The goal is to ensure that the information being reported is accurate and compliant with applicable laws.

Examples of issues that may lead someone to pursue credit repair include:

- Accounts that do not belong to them

- Duplicate accounts

- Incorrect balances

- Reporting errors

- Identity theft-related accounts

- Outdated negative information

- Collection accounts reported inaccurately

Credit repair is often associated with the Fair Credit Reporting Act (FCRA), which gives consumers the right to dispute inaccurate information appearing on their credit reports.

A key misunderstanding is that credit repair is not about removing accurate negative information simply because it is undesirable. If a late payment was legitimately reported and remains within the reporting period, it may continue to appear even if the consumer wishes it would disappear.

The purpose of credit repair is accuracy.

What Is Credit Building?

Credit building is different because it focuses on creating and strengthening positive credit history. Instead of correcting existing problems, credit building is about demonstrating responsible borrowing behavior over time. Lenders and scoring models want evidence that a consumer can manage credit responsibly. Credit building activities help create that evidence.

Examples include:

- Making on-time payments

- Maintaining low credit card balances

- Using credit consistently and responsibly

- Diversifying credit types when appropriate

- Avoiding unnecessary late payments

- Keeping older accounts open when practical

Unlike credit repair, which can sometimes produce results within weeks or months, credit building is usually a longer-term process with very few shortcuts. For example, a consumer who opens a secured credit card today may need many months of responsible use before meaningful improvements begin appearing in their credit profile.

Why Credit Repair Alone Is Often Not Enough

Many consumers focus entirely on repairing past issues while overlooking the need to build future credit strength. Even if every legitimate dispute is resolved successfully, a credit profile still needs positive information.

Imagine someone who removes an inaccurate collection account but has no active credit cards, no installment loans, and very little recent activity. Their credit report may be cleaner than before, but lenders still have limited information available to evaluate risk.

This is why many consumers eventually discover that credit repair and credit building often work together. Removing inaccurate information can improve the foundation, but building positive history helps strengthen the structure sitting on top of it.

Don’t Start Building Without Reviewing Your Reports

The opposite problem occurs as well. Some consumers spend years trying to build credit while never reviewing the information being reported about them. An identity theft account, incorrect balance, or reporting error can quietly undermine progress for years if it goes unnoticed.

As consumer awareness grows, more people are learning their credit rights and the importance of regularly reviewing credit reports for accuracy rather than assuming all reported information is correct. Building positive habits remains important, but those habits are most effective when the underlying information is accurate.

The Most Effective Approach Usually Involves Both

For many consumers, the best strategy is not choosing between credit repair and credit building. It is understanding when each is appropriate. Credit repair addresses problems. Credit building creates opportunities. One focuses on correcting the past. The other focuses on strengthening the future.

A healthy credit profile often requires both elements. Consumers benefit from reviewing their reports regularly, disputing inaccurate information when necessary, and simultaneously developing the habits that contribute to long-term credit success.

Consumers who understand the difference are often better positioned to make informed decisions, set realistic expectations, and develop a more effective strategy for improving their overall credit health. Whether someone is recovering from past financial difficulties, correcting reporting issues, or simply starting their credit journey, recognizing the role of both credit repair and credit building can provide a clearer path toward long-term financial stability.

{kind=link}