Picture this: It’s the last day of the month. Your phone buzzes with “Electricity bill due tomorrow – ₹2,347”. You sigh, open your banking app, scan a QR, type the amount, enter the UPI PIN… again. Now fast-forward to 2025. The same bill? Paid automatically at 12:01 am while you were fast asleep. No reminders, no late fees, no hassle. That, my friend, is the magic of the UPI Mandate – the quiet revolution that’s turning “I forgot to pay” into ancient history.

If you’ve ever googled “What is UPI Mandate?” at 11:55 pm while panicking about a SIP deduction, you’re not alone. Launched by NPCI in 2021 and supercharged with new features in 2024-25, the UPI Mandate (also called e-Mandate or standing instruction on UPI) is basically your digital “auto-pay genie”. You set it once, and money flies out of your account on the exact date, every single time – safely, instantly, and without you moving a muscle.

Ready to finally understand this game-changer? Grab a cup of chai; we’re going deep, but I promise to keep it fun.

What Exactly is a UPI Mandate?

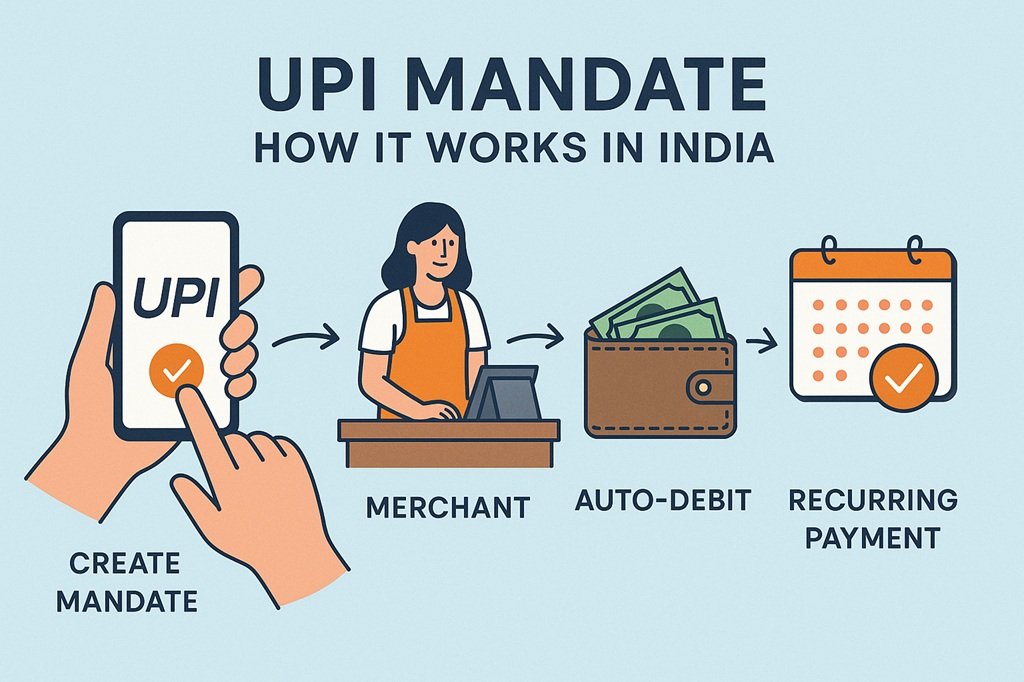

At its core, a UPI Mandate is a permission slip you give to someone (a merchant, utility company, mutual fund house, OTT platform, etc.) saying: “Hey, on this date every month/week/year, go ahead and pull this exact amount from my bank account using UPI. I trust you.”

Think of it as the love child of old-school ECS/NACH mandates and lightning-fast UPI. You get the reliability of direct debit but with the speed, transparency, and control that only UPI can offer.

Types of UPI Mandates Available Right Now

- One-time Mandate – Perfect for high-value purchases where the amount isn’t fixed (e.g., buying a phone on EMI where the last installment is smaller).

- Recurring Fixed Mandate – The classic. Netflix ₹199 every 1st? SIP ₹5,000 every 7th? This is your guy.

- Recurring Variable Mandate – Electricity bill changes every month? No problem. You set a maximum cap (say ₹5,000) and the actual amount is pulled.

- Revocable vs Irrevocable – Most are revocable (you can pause/cancel anytime). Some (like certain loan EMIs) might be irrevocable till maturity.

Why Is Everyone Suddenly Obsessed with UPI Mandate?

Because life’s too short to remember 27 different due dates, that’s why!

Jaw-Dropping Benefits You’ll Wish You Knew Earlier

- Zero late fees forever – Auto-debit happens on the dot. Say goodbye to “₹250 penalty” surprises.

- One-time setup, lifetime peace – Set it once in 30 seconds, forget it forever.

- Works even if you change phones – The mandate lives on NPCI servers, not your device.

- Pause or cancel anytime – Feeling broke this month? Hit pause from Google Pay/PhonePe in two taps.

- No more “Insufficient balance” drama – Most apps now send pre-debit notifications 24 hours before. Top-up in time, or the mandate simply skips (no penalty from NPCI side).

- Extra layer of safety – You authenticate the very first transaction with UPI PIN + OTP. Future debits? Just a server-to-server whisper (but you can block instantly if something feels off).

- Works across 400+ banks – Literally every bank that supports UPI supports mandates now.

- Free for customers – Banks don’t charge you (some merchants might, but rare).

How Does a UPI Mandate Actually Work Behind the Scenes?

Let’s walk through a real-life example – setting up your Spotify subscription.

- You open PhonePe → Bill Payments → Spotify.

- Choose “AutoPay” instead of “Pay Now”.

- Enter your VPA or scan the merchant’s mandate QR.

- The app shows: Amount ₹149 | Frequency: Monthly | First debit: 28-Nov-2025 | Max amount ₹199.

- You approve with UPI PIN (and sometimes OTP).

- Boom! Mandate created. You’ll get an SMS + app notification: “UPI Mandate created for Spotify – MANDATE123XYZ”.

- On 28th every month, ₹149 vanishes silently at 12:00 am. You get a debit SMS as usual.

That’s it. No standing in bank queues, no uploading cancelled cheques, no 15-day activation delay like the old NACH days.

The Tech Magic

- You → Merchant → Your Bank → NPCI → Sponsor Bank → Merchant’s Bank → Done!

- The first transaction is a normal UPI collect request (you approve).

- Subsequent ones are “mandate execute” requests that bypass customer intervention (but only within the limits you set).

Step-by-Step: How to Create Your First UPI Mandate

Whether you’re Team Google Pay, PhonePe, Paytm, BHIM, or banking app – the flow is almost identical.

Using Google Pay (the one I personally use)

- Open GPay → See All → Bills & Recharges.

- Pick category (Mobile Recharge, Electricity, OTT, etc.).

- Select the biller → Choose “Set up Autopay”.

- Enter details → You’ll see a “Create UPI Mandate” screen.

- Set frequency, amount/cap, end date (optional).

- Authenticate with UPI PIN.

- Done! You’ll see it under “Manage Autopay”.

Pro tip for variable bills (electricity, credit card)

Look for “Smart Limit” or “Dynamic Mandate” option – most apps rolled this out in 2024-25.

Where Can You Use UPI Mandate Right Now?

As of November 2025, literally thousands of merchants:

- OTT: Netflix, Spotify, Amazon Prime, Disney+ Hotstar, Zee5

- Utilities: All state electricity boards, BESCOM, Reliance Energy, Tata Power, water boards

- Telcos: Airtel, Jio, Vi postpaid & broadband

- Investments: Groww, Zerodha Coin, Kuvera, INDMoney SIPs

- Insurance: LIC, HDFC Life, ICICI Pru monthly premiums

- Loan EMIs: Bajaj Finance, Tata Capital, earlySalary

- Credit card bills: Some banks allow auto-pay via UPI mandate now (HDFC, Axis leading the pack)

- Even local kirana stores for “monthly ration credit” (yes, really!)

Managing, Pausing, or Killing a UPI Mandate When Life Happens

Changed jobs? Want to pause SIPs? Girlfriend mad because Netflix ate your date budget? Here’s your escape hatch.

How to View All Active Mandates

- Google Pay → Profile → Payment Methods → Manage UPI Autopay

- PhonePe → My Money → AutoPay

- Paytm → UPI & Payment Settings → Mandate Management

You’ll see every single mandate with:

- Merchant name

- Amount/Frequency

- Next debit date

- Options: Pause | Modify | Revoke

Revoking takes exactly 3 seconds and is instant – no waiting for merchant approval.

Common Myths About UPI Mandate – Busted!

Myth 1: “Someone can empty my account!” Reality: Impossible. You set the exact amount or cap. Even if a merchant goes rogue, they can’t pull more than you allowed.

Myth 2: “I lose control of my money.” Reality: You can block all future debits with one tap. Try doing that with old ECS!

Myth 3: “It works only for fixed amounts.” Reality: Variable mandates are live everywhere in 2025.

Myth 4: “My small-town bank won’t support it.” Reality: If your bank supports UPI, 99.9% chance they support mandates.

FAQs

Q: Is UPI Mandate safe?

A: Safer than handing over your debit card details. First transaction needs your PIN + OTP. Future ones are encrypted server-side, and you can freeze everything instantly.

Q: What if I don’t have money on the due date?

A: The transaction fails gracefully. Most billers retry 2-3 times over the next days. No NPCI penalty, though the merchant might charge late fees (check their policy).

Q: Can I set a UPI Mandate for someone else’s account (like parents’ electricity bill)?

A: Yes! Just use their VPA or registered mobile number during setup.

Q: Are there any charges?

A: Zero from banks/NPCI. A few merchants (some insurance companies) might charge ₹2-5 convenience fee – always shown upfront.

Q: Difference between UPI AutoPay and UPI Mandate?

A: They’re literally the same thing. Different apps just brand it differently.

Q: Can NRIs use UPI Mandate?

A: Absolutely, as long as their bank account is NRO/NRE and linked to UPI.

The Future: What’s Next for UPI Mandate?

By 2026, NPCI plans:

- UPI Mandate for credit cards (pay your card bill using another bank’s UPI – mind-blowing!)

- “Mandate on Credit” – pay later for subscriptions using credit line

- Voice mandates via UPI 123PAY for feature phones

- Cross-border recurring payments (imagine auto-paying your US Netflix from Indian account)

Conclusion

Let’s be real – adulting is hard enough without chasing 15 due dates every month. The UPI Mandate isn’t just a feature; it’s financial freedom in your pocket. One 30-second setup today can save you hundreds of rupees in late fees and hours of mental load every year.

So go ahead. Open your favorite UPI app right now. Find that one bill that always slips your mind. Set up your first mandate.

And when the 1st of next month rolls around and your phone quietly says “₹699 debited to Netflix”, smile. You’ve officially leveled up.

You’re welcome. 😊

{kind=link}