Have you ever placed an order to buy some shares online, only to check your account right away and see nothing there? It’s frustrating, right? You might think the deal happened instantly, but that’s not how it works. There’s a behind-the-scenes process called the settlement cycle that makes sure everything transfers smoothly between the buyer and the seller. In India, we’ve moved to a super-fast system called T+1, where things wrap up in just one day. This keeps trades secure and quick. But why does this matter to everyday investors like you or me? Let’s dive in and break it down step by step. We’ll look at what settlement really means, how it happens, the different timelines like T+1 or T+2, who’s involved, how it’s changed over time in India, the upsides, the potential downsides, and more. By the end, you’ll have a clear picture of this key part of stock trading.

Imagine you’re at a local market buying fruits from a vendor. You pick the apples, agree on the price, and hand over the cash. The vendor gives you the bag right then. That’s instant settlement. But in the stock market, it’s more like ordering online – you pay, but the delivery takes a bit because the system checks everything to avoid mix-ups. That’s the settlement cycle in a nutshell. It ensures no one gets cheated and that the market runs fairly for everyone.

Understanding Settlement Cycle in Simple Terms

Settlement is basically the final handover after a stock trade. When you buy shares, you’re not just clicking a button; you’re entering a deal where you get ownership of part of a company, and the seller gets your money. But it doesn’t happen on the spot because there are checks to make sure both sides can deliver what they promised.

Think of it like this: You agree to buy a used bike from a friend. You shake hands on the price (that’s the trade), but then you need to transfer the money, get the papers signed, and take the bike home (that’s settlement). In stocks, this handover involves electronic shares moving to your digital account, called a Demat account, and money going to the seller’s bank.

Why the delay? It’s to protect everyone. If the seller doesn’t have the shares or the buyer doesn’t have the funds, the system catches it early. Without settlement, trades could fall apart, leading to chaos. For instance, during busy market days, thousands of trades happen every minute. Settlement organizes all that mess into a clean transfer.

In real life, settlement affects how you plan your investments. If you’re a short-term trader, knowing when your money or shares arrive helps you decide your next move. Say you sell shares to buy something else – if settlement is slow, your cash is tied up, and you might miss a good opportunity.

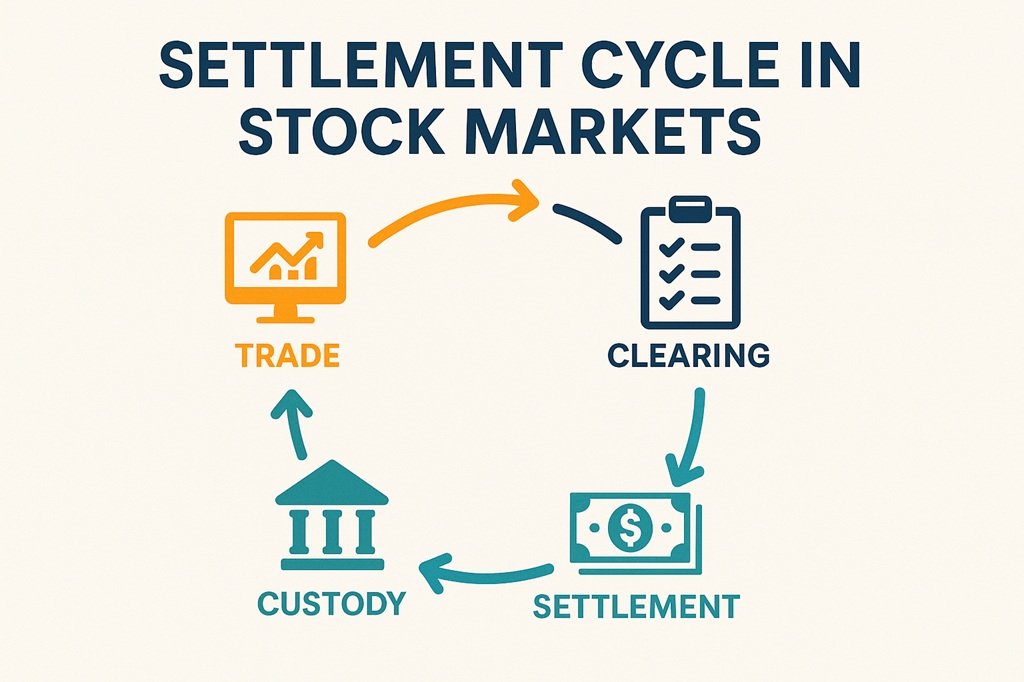

Step-by-Step: How the Process Works from Trade to Settlement

The journey from placing an order to seeing shares in your account has a few clear steps. Let’s walk through them one by one, with examples to make it real.

First comes Trade Execution. This is when your buy or sell order hits the stock exchange, like the National Stock Exchange (NSE) or Bombay Stock Exchange (BSE). The system matches your order with someone on the other side. For example, if you’re buying 100 shares of Reliance Industries at Rs 2,500 each, the exchange finds a seller offering at that price or better. It’s like an auction where buyers and sellers meet digitally. This happens in seconds during trading hours, usually 9:15 AM to 3:30 PM in India.

Next is Clearing. Here, a middleman called the clearing corporation steps in. Think of them as the referee. In India, it’s usually the National Securities Clearing Corporation Limited (NSCCL) for NSE or Indian Clearing Corporation Limited (ICCL) for BSE. They calculate what everyone owes. If you bought those Reliance shares, they check if you have enough money in your trading account. For the seller, they verify the shares are in their Demat. This step prevents defaults. An example: During the 2008 financial crisis, clearing helped spot risky trades early, saving markets from bigger crashes.

Then there’s Settlement. This is the actual transfer. Shares move from the seller’s Demat to yours via depositories like NSDL or CDSL, and money flows through banks. Under T+1, if you trade on Monday, everything settles by Tuesday end. Picture this: You buy shares on a Friday. Monday is a holiday? Settlement shifts to Tuesday. It’s all about business days, not weekends or holidays.

Finally, Custodial Confirmation. This is the wrap-up where your broker and depository confirm everything’s in place. Your app or statement shows the update. It’s like getting a receipt after delivery. In practice, if there’s a glitch, like insufficient funds, the exchange might penalize you or auction shares to cover it.

A real-world example: Suppose Raj, a Mumbai trader, buys 50 shares of HDFC Bank on Wednesday (T day). Under T+1, by Thursday evening, the shares are in his Demat, and the seller gets paid. If Raj sells them immediately on Thursday, he can use the cash for something else on Friday. This speed helps active traders flip investments quickly.

Key Components of the Settlement Cycle

Breaking it down further, the settlement cycle involves a few key players and steps. You’ve got the buyer, seller, brokers, clearing corporations (like NSE Clearing Ltd.), and depositories (NSDL or CDSL). They all work in sync, kinda like a well-oiled machine.

- Trade Execution (T Day): This is when the magic starts – you place your order, it matches with a seller, and boom, trade done.

- Clearing: Here, obligations are figured out. Who owes what to whom? Netting happens to simplify things.

- Settlement: The big finale – funds and securities move.

Breaking Down T, T+1, T+2, and Beyond

These “T” terms might sound technical, but they’re just timelines. “T” stands for Trade Day – the day the deal is struck.

T (Trade Date): This is ground zero. Your order executes, but nothing moves yet. All details go to the clearing house for processing. For instance, if you trade on October 9, 2025, that’s T. No shares or money change hands; it’s just recorded.

T+1 Settlement Cycle: India’s current standard, fully rolled out in January 2023. Settlement happens one business day later. Buy on Monday? Get shares Tuesday. This cut down wait times from older systems. Why the change? Faster cycles mean less risk if markets drop suddenly. Example: During COVID market swings in 2020, T+1 would have let investors access cash quicker to buy dips.

T+2 Settlement Cycle: The old way, used until 2023. Two days after trade. Trade Monday, settle Wednesday. It worked, but had issues like higher default risks. If a broker went bust in those two days, trades could fail. Many countries like the US still use T+1 or T+2, but India led by switching early. Drawback: Slower liquidity. Say you sell shares for an emergency – waiting two days hurts.

T+0 (Same-Day Settlement): The future is here, sort of. SEBI started a pilot in March 2024 with 25 stocks. By April 2025, it expanded to 500 more securities, and it’s optional alongside T+1. As of October 2025, it’s voluntary for select stocks, with plans to include top 500 gradually. Trades in the morning settle by evening. Imagine buying at 10 AM and having shares ready by 4 PM to sell if needed. It’s great for high-frequency traders but requires top-notch tech. Recent SEBI updates in October 2025 tightened rules for block deals in T+0, like minimum Rs 25 crore trades and specific windows (8:45-9:00 AM and 2:05-2:20 PM), to boost transparency.

Why these shifts? Shorter cycles reduce “settlement risk” – the chance something goes wrong between trade and handover. In volatile markets, like during the 2022 Ukraine crisis, quick settlements protected investors from big losses.

Key Players in the Settlement Game

Settlement isn’t a solo act; it’s a team effort. Here’s a closer look at each player, with examples of their roles.

- Investor: That’s you! You start it by placing orders via an app or broker. You need funds ready for buys or shares for sells. Example: If you’re short on cash, your trade might get rejected, like trying to buy a phone without money in your wallet.

- Broker: Your go-between, like Zerodha or Groww. They execute orders and handle paperwork. They ensure you comply with rules. For instance, if you forget to link your bank, the broker flags it.

- Stock Exchange (NSE/BSE): The marketplace. They match orders in real-time. During IPO rushes, like the LIC listing in 2022, exchanges handle millions of trades without hiccups.

- Clearing Corporation: The risk managers. They guarantee trades even if one side fails. NSCCL, for example, uses margins (like deposits) to cover defaults. In 2019, a broker default was handled smoothly thanks to them.

- Depository (NSDL/CDSL): Digital vaults for shares. They transfer electronically, no paper. When you convert physical shares to Demat, they store them safely. Example: During Demat booms post-2020, CDSL added millions of accounts.

- Banks/Payment Gateways: Handle money moves. UPI or NEFT ensures quick transfers. If a bank delays, settlement could slip, but rules penalize that.

All these work like a relay race, passing the baton smoothly.

How India’s Settlement Cycle Evolved Over Time

India’s stock market wasn’t always this slick. It’s come a long way from paper chaos to digital speed.

Back in the 1980s and early 1990s, everything was physical. Shares were paper certificates, mailed around. Settlements took weeks – T+14 was normal! Payments by cheque added delays. The 1992 Harshad Mehta scam exposed flaws: Fake bank receipts led to a crash. This pushed reforms.

By 2001, SEBI introduced T+5: Settle in five days. It cut risks but was still slow. Then T+3 in 2002 sped things up, building trust after the dot-com bust.

In 2003, T+2 arrived, aligning with global norms. Brokers got cash faster, boosting trading volumes. But the real game-changer was Demat in the late 1990s. NSDL launched in 1996, CDSL in 1999. No more lost certificates – everything electronic. This slashed fraud and sped settlements.

Post-2008 crisis, tech upgrades like online platforms made things seamless. By 2021, SEBI eyed T+1 to lead globally. Phased in from 2022: Small stocks first, all by 2023. It reduced locked funds by 50%, per SEBI data. Example: In 2023 bull run, T+1 let investors rotate money quickly into rising stocks like Adani.

Now, T+0 is rolling out. Pilot in 2024, expanded in 2025 to over 500 stocks. It’s optional, but SEBI’s October 2025 block deal tweaks show commitment to efficiency. Compared to the US (T+1 since 2024) or Europe (T+2), India’s ahead. This evolution turned a clunky system into a world-class one, attracting foreign money – FDI in stocks hit records in 2024.

Why Shorter Cycles Are a Big Win: Benefits Explained

Shifting to shorter settlements like T+1 and T+0 brings tons of perks. Let’s unpack them with everyday examples.

Quicker Cash Flow: Money or shares arrive faster. Sell today, reinvest tomorrow. For retirees relying on dividends, this means less waiting. In T+2 days, funds were stuck; now, they’re free sooner, boosting market activity by 20-30%, as per exchange reports.

Lower Risks: Less time for things to go wrong. If markets crash overnight, you’re not exposed as long. During 2020’s COVID dip, quicker settlements could have saved billions in losses. Counterparty risk drops – if a broker defaults, impact is minimal.

Better Liquidity: More trades happen as capital circulates fast. Small investors benefit: Sell shares for a home downpayment without delays. Market volumes rose post-T+1, making prices fairer.

Efficiency Boost: Automation cuts costs. Brokers save on holding margins. For the system, fewer errors mean smoother ops. Example: Clearing houses process trades 50% faster now.

Global Edge and Trust: India’s speed draws investors. Foreign funds poured in after T+1, per RBI data. It builds confidence – no more worries about delays in a fast world.

Overall, it’s like upgrading from a bicycle to a car: Faster, safer, more fun.

Risks and Challenges in Settlement

Nothing’s perfect. Shorter cycles have hurdles too. Here’s what to know, with tips to handle them.

Tight Timelines: T+1 gives little wiggle room. Miss funding? Trade fails. For newbies, this means planning ahead. Example: During festivals, bank holidays can mess up schedules – always check calendars.

Failure Risks: Short on funds or shares? Auction time. Sellers might lose if prices drop. In 2023, some retail traders faced penalties for overselling without holdings. Tip: Use broker alerts for balances.

Global Hitches: Foreign investors deal with time zones. A US trader buying Indian stocks might struggle with same-day wires. Currency conversions add complexity. SEBI’s easing rules, but it’s still a pain.

Tech Glitches: Everything’s digital, so hacks or outages hurt. The 2021 NSE glitch delayed trades. Cyber risks rise with speed. Solution: Exchanges invest in backups, but investors should diversify brokers.

Liquidity Squeeze: Big players need cash ready fast. Small brokers might struggle. During 2022 inflation, some faced crunches.

To mitigate: Educate yourself, use reliable brokers, and keep buffers. Regulators like SEBI monitor to keep things stable.

Why Settlement Matters to You

The settlement cycle is the quiet hero of the stock market, turning promises into reality. From slow paper days to T+1 and emerging T+0, India’s journey shows smart reforms at work. It makes trading safer, faster, and more inclusive. Whether you’re a day trader flipping stocks or a long-term holder building wealth, understanding this helps you navigate better. As India pushes boundaries – with T+0 expanding in 2025 – we’re set for even smoother sails. Remember, knowledge is power; stay informed, trade smart, and watch your portfolio grow.

Frequently Asked Questions

Q1. What exactly is a settlement cycle in stocks?

It’s the timeline for transferring shares to buyers and money to sellers after a trade.

Q2. What does T+1 really stand for?

Trade plus one day – settlement on the next business day.

Q3. Is T+1 active everywhere in India now?

Yes, since January 2023 for all equity trades.

Q4. How’s T+1 different from T+2?

T+1 is one day faster, cutting risks and speeding cash flow.

Q5. What’s the deal with T+0?

Same-day settlement, optional for select stocks as of 2025, expanding gradually.

Q6. Can settlement fail, and what happens then?

Yes, if funds/shares are missing. Exchanges auction to cover, with penalties.

Q7. How does this affect foreign investors?

Time zones and forex can complicate, but SEBI’s making it easier.

Q8. Why did India switch to shorter cycles?

To reduce risks, boost efficiency, and attract global money.

Q9. What’s a Demat account’s role here?

It holds electronic shares, making transfers quick and safe.

Q10. Any tips for new traders on settlement?

Keep funds ready, check holidays, and use apps for real-time updates.

Conclusion

Wrapping up, the settlement cycle in India’s stock markets is that crucial workflow keeping everything ticking smoothly. From the standard T+1 to the zippy optional T+0, it’s all about speed and safety. We’ve covered the basics, history, steps, impacts – hopefully, it’s clearer now. Whether you’re a newbie dipping toes or a seasoned player, grasping this cycle empowers better decisions. After all, in investing, timing’s everything! Keep an eye on SEBI updates; who knows, instant settlements might be next. Happy trading, folks – may your portfolios soar.

{kind=link}