Kisan Vikas Patra is re-launched by government on 18th Nov, 2014. Main reason of re-launching KVP back is to boost house hold saving rate. Once upon a time KVP was very famous investment option. Let’s see what features KVP offers to investors.

Kisan Vikas Patra Features

- Double your money in 8 years and 4 months

- Interest Rate offered – 8.7%

- Minimum Investment 1000 Rs/- Maximum investment No limit

- No Tax Benefit

- Interest earned on maturity is taxable

- Lock period for 2 years and 6 months

- Investment can be done by Individual only

- Single and Joint option possible in KVP

Kisan Vikas Patra is Beneficial for Whom?

Kisan Vikas Patra is beneficial for rural area, mainly to people who don’t have facility of banking. You don’t need any bank account to invest in Kisan Vikas Patra. KVP can be purchased by cash also. It is possible to transfer KYC also. Rural People and farmer can take benefit of this scheme however for Urban Investor many other options are available.

Other Superior Investment Option Compare to KVP

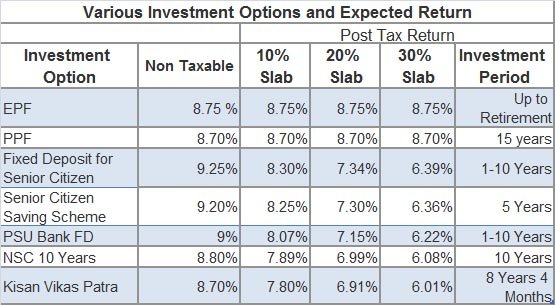

PPF

Kisan Vikas Patra gives returns of 8.7% and doubles money in 8 years 4 months. Compare to KVP, PPF also offers 8.7% return but it is tax free. In Kisan Vikas Patra we have no limit on investment while in PPF we have maximum limit of 1.5 Lac.

Senior citizen saving scheme

Senior citizen saving scheme offers 9.2% return and it also offers tax benefit under 80C. Post tax deduction return in senior citizen saving scheme is also higher compare to Kisan Vikas Patra.

Fixed Deposit or FMP

Smart investor can prefer investment in fixed deposit, FMP or corporate fixed deposit compare to KVP. Fixed deposit offers nearly 9% return. Post tax deduction return in fixed deposit is higher compare to KVP.

Should I invest in KVP?

KVP is typical post office type scheme which offers fixed return and no tax benefit. Smart investor will not invest in KVP. Smart investor will have other better investment options like Equity, FMP, FD, PPF etc.