The NRIs (Non-Resident Indians) are confused when it comes to taxation issues especially related to rented income, a sale of real estate and other investments etc. Here is a complete guide to explain about tax implication for NRIs.

One of my friends has recently moved to Canada. He has income from property in India. Apart from that, he has income from other sources in India. He wants to know about the applicability of income tax for NRI. He is also confused about filing Income tax return. So, in this post, let’s try to address common tax related queries asked by NRI.

Who is considered as NRI?

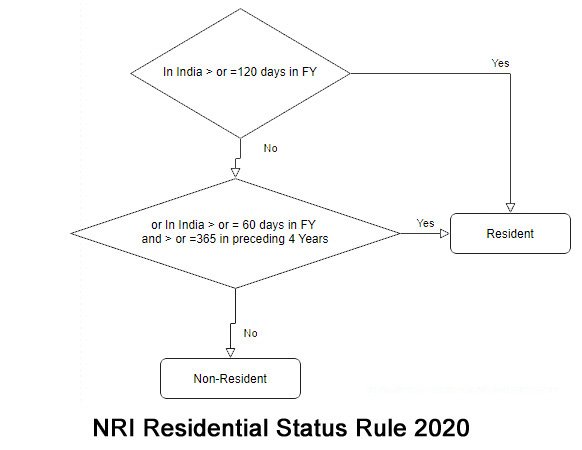

Residential rule for NRI is changed in Budget 2020.

An individual or manager of HUF who is non-resident in India in 7 out of 10 preceding years will be regarded as “not ordinary resident” in India.

NRI who is a citizen of India if visiting India for more than 120 days in a year will lose his non-residential status (earlier this limit was of 182 days). In the simple words if Indian national wants to claim NRI status he cannot stay in India above 120 days. (4 months). This means you need to stay minimum 245 days abroad for claiming your NRI status.

For residential status only above condition is added, remaining conditions remain same.

In addition to above condition, if person is not staying in India for greater than 60 days in the financial year or 365 in preceding four financial year status can be claimed as NRI.

If these conditions do not get satisfied residential status will be ordinary Resident. The flow chart of explaining NRI status is given below.

Also Read – RNOR Status NRI can save Tax up to 3 Years

Income Tax for NRI – Taxable Income of an NRI

Your resident status will decide your income tax liability in India. If your status is ‘resident’ your global income is taxable in India. If your status is ‘NRI’ your income earned in India is taxable in India.

Following incomes are taxable for NRI –

Income from Salary

If you are NRI and you receive a salary in India or someone receives it on your behalf, you are liable to pay income tax on such salary. This means if you render service outside India and accept a salary in India, you need to pay income tax on salary income.

E.g Mr.Suresh Works in IT firm. IT firms take a project in Dubai and depute Mr.Suresh for project work. Mr.Suresh opt to take a salary at India. Mr.Suresh is liable to pay tax on salary income.

Rental Income

The most common source of income of NRI is rental income. Most of NRI rent out their properties and receive monthly rental income. Any income arising from rental property for NRI is taxable in India. This income is taxed as per income tax slab rates.

A tenant who pays rent to an NRI needs to deduct TDS at 30%. A tenant needs to prepare 15CA and submit it online to the income tax department. This is irrespective of payment is made in bank account located in India or at abroad.

Income from Other Sources

Income from any other sources in India is taxable for NRI. Few examples of other sources include interest income earned on NRO bank account, fixed deposit etc. The interest earned on NRE or FCNR account is not taxable.

In short as an NRI you need to sum up all income originated in India or received in India. If your total income in India is crossing income tax threshold limit you need to pay Income tax.

Also Read – To do list for NRI before leaving India

Income from Business and Profession

NRI is also liable to pay tax on any income arising due to business and profession in India. This means if you have business setup in India or controlled in India you are liable to pay tax.

Long term Short term capital Gain – Income from Capital Gain

NRI is also liable to pay long-term capital gain tax and short-term capital gain tax. This means any capital gain arising due to a transfer of capital asset which is situated in India shall be taxable in India. However, the certain special tax treatment is offered for specific investments. The tax rate applicable on such investment is 20% provided NRI has no other income except special investment during the financial year. The special investment includes following investment type.

- Shares in Indian companies

- Debentures issued by a public-listed Indian company

- Deposits with a bank and public companies

- Central government securities

Deduction for such investment is not considered under 80C for NRI. However, in case of long-term capital gain, one can avail an exemption on the profit under section 115F.

Deduction and Exemptions Applicable to NRI

After looking at a taxable income of NRI, let’s take a look at deduction and exemptions applicable to NRI.

- Most of the deductions under 80 C are allowed to NRI. Some examples are insurance premium, children tuition fees, principal repayment for a home loan, ULIP investment and Investment in ELSS.

- NRI is also allowed to claim deduction under 80D for a premium paid for health insurance policy.

- NRI can claim a deduction for the interest payment on education loan. The loan may be for the higher education of NRI or for spouse and children.

- Another deduction which is allowed to NRI is under section 80G which is for the donation made under a social cause.

- NRI can also take benefit of 80 TTA. It is towards interest income on saving bank account. The maximum limit is Rs.10000.

Also Read – Top 5 Best Investment Options for NRI in India

When NRI is required to file Income Tax Return?

One of the most frequently asked question by NRI is – Do I need to file Income tax return? Well, NRI needs to file Income Tax Return under following conditions –

- If Total Income is crossing taxable limit during a financial year. This means as per current rule if total income of NRI in India is above 2.5 Lakh, one need to file Income tax return.

- If TDS is deducted from your Income and you are looking for refund as your income is below taxable limit.

- If you have Short term Capital Gain (STCG) or Long term Capital Gain(LTCG) from sale of assets or investments in India even if your income is below basic exemption limit.

- Suppose you want to carry forward and set off any losses against gains.

- If you want to claim tax benefit under tax treaty even though your income in India is below threshold limit.

{kind=link}